Capacity-Based Monetary Theory and the September 11 Shock: A Macro-Institutional Assessment

Introduction: The Ontological Reassessment of Sovereign Value

The fundamental question of what constitutes money and how it derives its value has persistently bedeviled economists, jurists, and philosophers. Traditional macroeconomic paradigms frequently rely on functional definitions—characterizing money as a medium of exchange, a unit of account, and a store of value. While these tripartite functional definitions describe the symptoms and utility of "moneyness," they fail to adequately explain the ontological asset structure that underpins a fiat currency. In the double-entry bookkeeping of a sovereign civilization, money appears strictly as a liability on the balance sheet of the state. It is a circulating promissory note. However, a liability cannot exist in a theoretical vacuum; it must be balanced by a corresponding asset. Capacity-Based Monetary Theory (CBMT) posits that the asset backing the liability of a modern fiat currency is not gold, nor the mere coercive decree of the state, but rather the Expected Future Impact of the society that issues it.

Under the CBMT framework, money is rigorously redefined as a floating-price claim on the future productive capacity of an economy. When an economic agent accepts a currency in exchange for current tangible goods or services, they are essentially acquiring a call option on the aggregate future labor of that society. They are executing a probabilistic bet that the society will possess the capacity—both physical and institutional—to redeem that claim for real value at a later date. This paradigm effectively extends Adam Smith's classical concept of "Labor Commanded," which dictates that the true value of a commodity is equal to the quantity of labor it enables the possessor to purchase or command.

The events of September 11, 2001, represent one of the most profound exogenous shocks to the economic and institutional structure of the United States. Traditional analyses of this tragedy typically focus on immediate capital destruction, localized employment impacts in lower Manhattan, and the short-term aggregate demand shocks resulting from halted commerce. However, to fully grasp the systemic, long-term alterations to the economic trajectory of the United States, a more robust ontological framework is required. This report applies the rigorous mathematical and theoretical framework of Capacity-Based Monetary Theory to model the macroeconomic and institutional shocks of September 11. Furthermore, it systematically analyzes the effectiveness of the unprecedented legislative and structural responses enacted by the United States government, specifically the USA PATRIOT Act and the creation of the Department of Homeland Security (DHS). By utilizing the mathematical specifications of CBMT—including the Augmented Solow-Swan model, the Institutional Realization Rate, and the Hamilton Filter—this analysis evaluates how the sovereign state's attempt to restore institutional order fundamentally altered the economy's production function. Finally, the report conducts an exhaustive discrepancy analysis, comparing the theoretical predictions generated by CBMT against the real-world macroeconomic data observed between 2000 and 2006, thereby identifying the limitations of the model in a globally integrated, hegemon-dominated financial system.

The Production of Impact and the Augmented Solow-Swan Framework

To evaluate the events of September 11 through the lens of CBMT, it is necessary to first establish the mathematical foundations of the theory. CBMT posits that the value of money is inextricably linked to the magnitude of real output, or "Impact" ($Y$). Impact encompasses the tangible goods, services, and innovations that a society produces. If the money supply remains constant while the capacity to produce impact expands, the purchasing power of money increases, resulting in deflation. Conversely, if the productive capacity degrades while the claim structure (the money supply) remains fixed, the value of the claim is inherently diluted, manifesting as inflation. Therefore, the "price" of money serves as a continuous, real-time index of the economy's underlying production function.

The starting point for quantifying this impact is the neoclassical growth model. However, CBMT argues that the standard Solow-Swan model is insufficient for modern fiat currencies because it treats human capital merely as an undifferentiated component of raw labor. To accurately model the "collateral" of a modern advanced economy like the United States, CBMT integrates the Augmented Solow-Swan model, specifically the Mankiw-Romer-Weil (1992) specification. This framework treats Human Capital ($H$) as an independent factor of production with its own accumulation and depreciation dynamics. The rigorous production function for Impact is defined as:

$$Y = K^\alpha H^\beta (AL)^{1-\alpha-\beta}$$

Where: $Y$ represents total production or "Impact," the underlying collateral of the currency. $K$ represents the stock of physical capital. $H$ represents the stock of Human Capital, encompassing skills, advanced education, and health. $L$ represents the aggregate labor force. $A$ represents labor-augmenting technology, or "Efficiency Capacity." $\alpha$ and $\beta$ represent the elasticities of output with respect to physical and human capital, respectively.

Crucially, the condition $\alpha + \beta < 1$ implies diminishing returns to broad capital accumulation. This specification demonstrates that a currency's strength depends heavily on the investment rate in human capital required to maintain the stock of $H$. Unlike a simple multiplier, human capital is a distinct asset class that constantly depreciates and requires perpetual replenishment. Money, therefore, is a systemic bet on the society's ongoing ability to maintain high levels of Human Capital ($H$) and Efficiency ($A$).

The Micro-Foundations of Human Capital and the 9/11 Shock

While the Mankiw-Romer-Weil specification provides the macro-equation for capacity, Gary Becker's theories provide the micro-foundation. Becker argued that labor is not a fungible, homogeneous commodity, but rather a form of capital accumulated through deliberate investment. His "Theory of the Allocation of Time" suggests that individuals combine market goods and their own time to produce commodities and economic impact. A currency backed by a population with high levels of advanced education represents a claim on a vastly larger pool of potential future impact.

The attacks of September 11 constituted an immediate, violent contraction of both physical capital ($K$) and human capital ($H$). The destruction of the World Trade Center complex resulted in severe physical property damage and cleanup costs, estimated to total between \$33 billion and \$36 billion. More critically within the Beckerian micro-foundation of CBMT, the loss of nearly 3,000 lives represented an acute, highly concentrated shock to Human Capital. The discounted value of the deceased workers' expected future earnings alone was calculated at approximately \$7.8 billion, representing an average of \$2.8 million in lost future impact per worker. Furthermore, the immediate macroeconomic fallout of the attacks temporarily reduced U.S. real GDP growth in 2001 by 0.5% and increased the unemployment rate by 0.11%, equating to an immediate reduction in active labor ($L$) by 598,000 jobs.

However, within the context of a multi-trillion-dollar national economy, the absolute physical and human capital reductions were statistically marginal. As noted in retrospective macroeconomic assessments, the isolated loss of lives and property on September 11 was not large enough to have had a measurable, permanent effect on the aggregate productive capacity of the United States on its own. Therefore, the profound and enduring macroeconomic shifts that followed the attacks cannot be explained merely through the destruction of $K$ and $H$. Instead, the true systemic shock occurred within the institutional and frictionless parameters of the CBMT framework.

The Hobbesian Trap and the Institutional Realization Rate

In the Capacity-Based Monetary Theory framework, theoretical production capacity is entirely irrelevant if the fruits of labor cannot be secured. The "hardware" of impact ($Y$) requires the "software" of robust legal and institutional frameworks to function. Thomas Hobbes classically described the "state of nature" as a condition of perpetual war, where life is "solitary, poor, nasty, brutish, and short". In rigorous economic terms, the Hobbesian state represents a regime characterized by infinite transaction costs.

Money cannot exist in a Hobbesian state. Because money is inherently a claim on the future, if the future is characterized by violence, expropriation, and radical uncertainty, the discount rate applied to future claims becomes effectively infinite. No rational economic agent would exchange a tangible, present good for a token promising a good tomorrow if "tomorrow" brings the likelihood of death or theft. Therefore, the very existence and value of money are predicated entirely on the strength of the Social Contract. The "Leviathan"—the sovereign state—must impose order to artificially lower transaction costs. The fundamental value of a fiat currency is, therefore, a continuous market pricing of the Leviathan's effectiveness at maintaining this order.

CBMT formalizes this relationship by utilizing the insights of Douglass North regarding transaction costs and institutional economics, proposing an Institutional Realization Rate ($IR$). The $IR$ is a coefficient ranging between 0 and 1, defined as:

$$Y_{realizable} = Y_{MRW} \times IR$$

Where $Y_{MRW}$ is the theoretical output predicted by the Mankiw-Romer-Weil model, and $IR$ is the measure of Institutional Quality, encompassing the rule of law, contract enforcement, and physical security. In a highly stable, high-trust society, the $IR$ approaches 1, meaning theoretical capacity is fully realizable. In a failed state experiencing civil war or anarchy, the $IR$ approaches 0, and even with vast natural resources and labor, the realizable impact collapses, taking the currency down with it.

The terrorist attacks of September 11 represented a sudden, catastrophic degradation of the U.S. Institutional Realization Rate. The revelation of unprecedented domestic vulnerability shattered the baseline assumption of sovereign security that underpins the U.S. dollar. The immediate aftermath saw commercial aviation entirely grounded, borders tightly restricted, and major financial markets, including the New York Stock Exchange, forced to close for days. This immediate suspension of the mechanisms of commercial and financial exchange represented an acute plunge in the $IR$ coefficient. Theoretical capacity ($Y_{MRW}$) remained largely intact outside of lower Manhattan, but it could no longer be fully realized into tangible economic impact ($Y_{realizable}$) due to the sudden spike in frictional transaction costs and existential fear.

The Hamilton Filter: Valuing Currency in a Stochastic Regime

Traditional deterministic macroeconomic models frequently fail to account for the sudden risk of the social contract breaking. To accurately price the value of money in a stochastic world prone to exogenous shocks, CBMT employs the Hamilton Filter. The Hamilton Filter, pioneered by James D. Hamilton in 1989, is the standard econometric algorithm for estimating discrete, unobserved regime shifts in time series data.

In the CBMT framework, the fundamental value of money is highly dependent on the probability of the economy operating in a specific state or regime ($S_t$), such as a "Stable Regime" (where $IR \approx 1$) versus a "Collapse Regime" (where $IR \to 0$). The filter recursively estimates the probability of the unobserved state using a prediction step, projecting probabilities forward based on transition matrices, and an update step, which adjusts the probabilities as new data ($y_t$) arrives. The mathematical foundation relies on determining when structural shifts occur and estimating the state transition probabilities governed by a Markov chain.

On the morning of September 11, the global market's collective, internal Hamilton Filter detected an immediate, violent shift in the transition matrix. The probability of the U.S. economy entering a "Collapse Regime" spiked dramatically. In the architecture of CBMT, when the Hamilton Filter detects such a regime shift—suggesting that the Leviathan may be losing control of its monopoly on security—the discount rate spikes, and the demand to hold claims on the future evaporates. The immediate behavioral response of businesses and consumers was entirely rational under this model: economic agents aggressively moved capital from illiquid, future-dependent assets (like equities and long-term bonds) into liquid, present-value assets like cash and checking accounts. Blue Chip Consensus GDP growth forecasts for 2001 were aggressively revised downward from 1.6 percent to 1.1 percent within a month of the attack, reflecting the market's rapid Bayesian updating of regime probabilities.

The Leviathan's Response: Legislation as Structural Friction

Faced with a collapsing Institutional Realization Rate and a Hamilton Filter pointing ominously toward a high-risk regime, the sovereign state was forced to act aggressively to restore the perception of the social contract and lower the probability of future violence. The Leviathan's response took the form of sweeping legislative, intelligence, and bureaucratic overhauls, most notably the USA PATRIOT Act and the Homeland Security Act.

However, according to CBMT, the restoration of $IR$ through coercive state security measures is not cost-free. In fact, it frequently requires the imposition of massive, permanent transaction costs that operate as a structural tax on the "Efficiency Capacity" ($A$) of the economy. While the state may successfully prove it is not a Hobbesian failure, the methods it uses to secure the future can fundamentally degrade the efficiency of generating that future.

The USA PATRIOT Act and Financial Transaction Costs

Passed with overwhelming bipartisan support and signed into law on October 26, 2001, the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism (USA PATRIOT) Act drastically expanded the surveillance and investigative powers of federal law enforcement and intelligence agencies. While the Act is frequently debated in the context of constitutional law and civil liberties, its most profound and enduring economic impact stems from Title III, which imposed stringent Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations on the global and domestic financial sectors.

Prior to 9/11, routine domestic financial transactions carried relatively low regulatory overhead, allowing for high-velocity capital allocation. The Patriot Act effectively drafted the private financial sector into the vanguard of the national security apparatus, significantly expanding the scope of institutions required to monitor, record, analyze, and report suspicious activities. This mandate was not limited to large commercial banks; it extended to mutual funds, credit card operators, broker-dealers, futures commission merchants, and small credit unions.

The macroeconomic transaction costs of these provisions were staggering and enduring. The Financial Crimes Enforcement Network (FinCEN) predicted that advanced Customer Due Diligence (CDD) rules alone would cost banks and their customers between \$700 million and \$1.5 billion over a decade, utilizing a "conservative" estimate of \$10 billion for broader regulatory impact studies. Individual large banks estimated their annual compliance costs to range between \$20 million and \$50 million, while midsize banks pegged costs at \$3 million to \$5 million annually.

Viewed strictly through the CBMT framework, these compliance costs represent pure deadweight loss—a structural degradation of the labor-augmenting technology and efficiency variable ($A$) in the Mankiw-Romer-Weil equation. Highly educated labor and advanced capital that could have been deployed toward productive, yield-generating investments were instead diverted into massive regulatory compliance departments, transaction monitoring software systems, and legal consulting. As highlighted by the National Association of Manufacturers and the Securities Industry Association, over 93 percent of compliance costs in the U.S. financial sector are labor-related, indicating a massive diversion of human capital ($H$) away from impact generation.

Furthermore, the implementation of the Patriot Act created an asymmetric wealth redistribution within the banking sector. Empirical studies utilizing comprehensive Call Report data from the Federal Financial Institutions Examination Council (FFIEC) demonstrate that AML compliance costs are characterized by significant economies of scale. Smaller community banks incurred a disproportionately higher compliance burden relative to larger, globally integrated institutions. Banks with assets under \$100 million reported compliance costs averaging almost 10 percent of their total noninterest expense, effectively double the relative burden experienced by the largest community banks. This regulatory friction accelerated industry consolidation, reduced new bank formation, and constrained capital access for local entrepreneurs. By raising the baseline cost of verifying trust, the Leviathan inadvertently degraded the efficiency of capital allocation across the lower tranches of the economy.

The Homeland Security Apparatus and the O-Ring Filter Degradation

In addition to erecting a massive financial surveillance apparatus, the federal government fundamentally restructured its physical security architecture. In March 2003, the Department of Homeland Security (DHS) was created, amalgamating 22 disparate federal agencies and offices under a single cabinet-level department. A central, highly visible component of this reorganization was the federalization of airport security through the creation of the Transportation Security Administration (TSA).

The creation of the DHS and the TSA introduced massive, systemic transaction costs to the physical movement of human capital ($H$) and goods. In the immediate aftermath of 9/11, U.S. exports of travel services (representing foreign tourists visiting the United States) dropped by 12 percent in 2001 and an additional 4 percent in 2002. Visa restrictions, enhanced border checkpoints, and continuous flow-control measures at commercial airports severely constrained the velocity of labor and international trade.

The operations of the TSA require immense annual funding, largely subsidized by direct frictional taxation on travel. The September 11 Security Fee, collected directly from airline passengers, generated roughly \$995 million in 2002. This fee scaled rapidly alongside the bureaucracy, generating \$1.86 billion by 2005, and is projected to exceed \$4.5 billion annually by 2025. Beyond the direct financial extraction, the TSA introduced severe time-based frictional costs that ripple through the macroeconomy. Increased passenger screening delays, rigorous inspection of supply-chain cargo, and strict customs protocols elevated the baseline costs of transport, insurance, and logistics handling.

Within the CBMT paradigm, the generation of elite, high-value economic impact relies heavily on the agglomeration and rapid mobility of human capital. CBMT utilizes Michael Kremer’s "O-Ring Theory of Economic Development" to explain how high-skill workers cluster together in complex production processes to maximize serendipitous synergy and output. By introducing permanent, unpredictable delays into the national aviation and logistics network—where "flow control" measures routinely delay private and commercial flights for hours due to air traffic control staffing shortages and security protocols —the DHS structurally lowered the efficiency parameter ($A$) of the entire U.S. production function. Businesses currently face longer delays at airports and land-border crossings, resulting in augmented insurance fees and reduced overall trade flows.

Evaluating Legislative Effectiveness: Cost-Benefit and Signaling Theory

To objectively evaluate the effectiveness of the Patriot Act and the DHS through the CBMT lens, one must weigh the perceived restoration of the Institutional Realization Rate ($IR$) against the permanent drag imposed on efficiency ($A$) and the diversion of physical capital ($K$).

The Failure of Cost-Benefit Proportionality and Deadweight Loss

From a strict economic cost-benefit perspective, the legislative response was vastly disproportionate to the statistical threat. The cumulative increase in US. domestic homeland security expenditures over the decade following 9/11 exceeded \$1 trillion. However, as researchers John Mueller and Mark G. Stewart have exhaustively documented, security-focused regulations implemented by the DHS have largely been exempt from the rigorous, standardized benefit-cost analyses routinely required for major federal regulations in areas such as environmental protection or transportation safety.

To mathematically justify these enhanced expenditures on a purely economic basis—even using analyses that substantially bias the consideration toward security—the implemented measures would have to prevent, deter, or foil 1,667 otherwise successful terrorist attacks per year (equating to more than four major attacks per day), with each attack inflicting \$100 million in damage. Alternatively, they would need to foil 167 attacks per year inflicting \$1 billion in damage each. This vast discrepancy reveals a severe case of "probability neglect" among policymakers, who focused almost exclusively on worst-case scenarios, inflated terrorist capacities, and assessed relative rather than absolute risk.

The opportunity costs of these expenditures were profound. The estimated \$32 billion per year in direct opportunity costs represented capital that could have been invested in domestic infrastructure, basic scientific research, or education—the exact factors that build Human Capital ($H$) and Technology ($A$). By diverting labor and capital resources away from productive private sector activities and toward reactive, less productive anti-terrorist activities, the legislation initiated a long-term suppression of the nation's baseline productivity growth rate.

Zahavi’s Handicap Principle and the Pricing of Capacity

If the economic cost-benefit analysis fails so dramatically, why did the Leviathan pursue such an inefficient path? CBMT resolves this paradox through the integration of Signaling Theory, specifically Amotz Zahavi’s Handicap Principle. The Handicap Principle posits that signals of strength are only reliable if they are differentially costly—meaning they require the "burning" of capital that a weaker entity could not survive.

When the United States established the DHS, passed the Patriot Act, and launched the broader Global War on Terror, it was engaging in a highly rational, albeit massively expensive, Proof of Surplus Capacity. The signal to the global Hamilton Filter was clear: the United States had generated enough past impact to accumulate vast surplus capital, and it implicitly possessed high confidence in its future ability to replenish it, even while burning trillions of dollars on domestic security theater and overseas military deployments. A low-capacity, failing state could not afford to ground its aviation system, restructure its banking sector, and launch global wars without jeopardizing its very survival. Thus, the massive deadweight loss of the homeland security apparatus served as a costly signal that successfully separated the U.S. Leviathan from actual failed states, forcibly manipulating the Hamilton Filter back toward a "Stable Regime" probability.

The Erosion of the Social Contract: Longitudinal Trust Decay

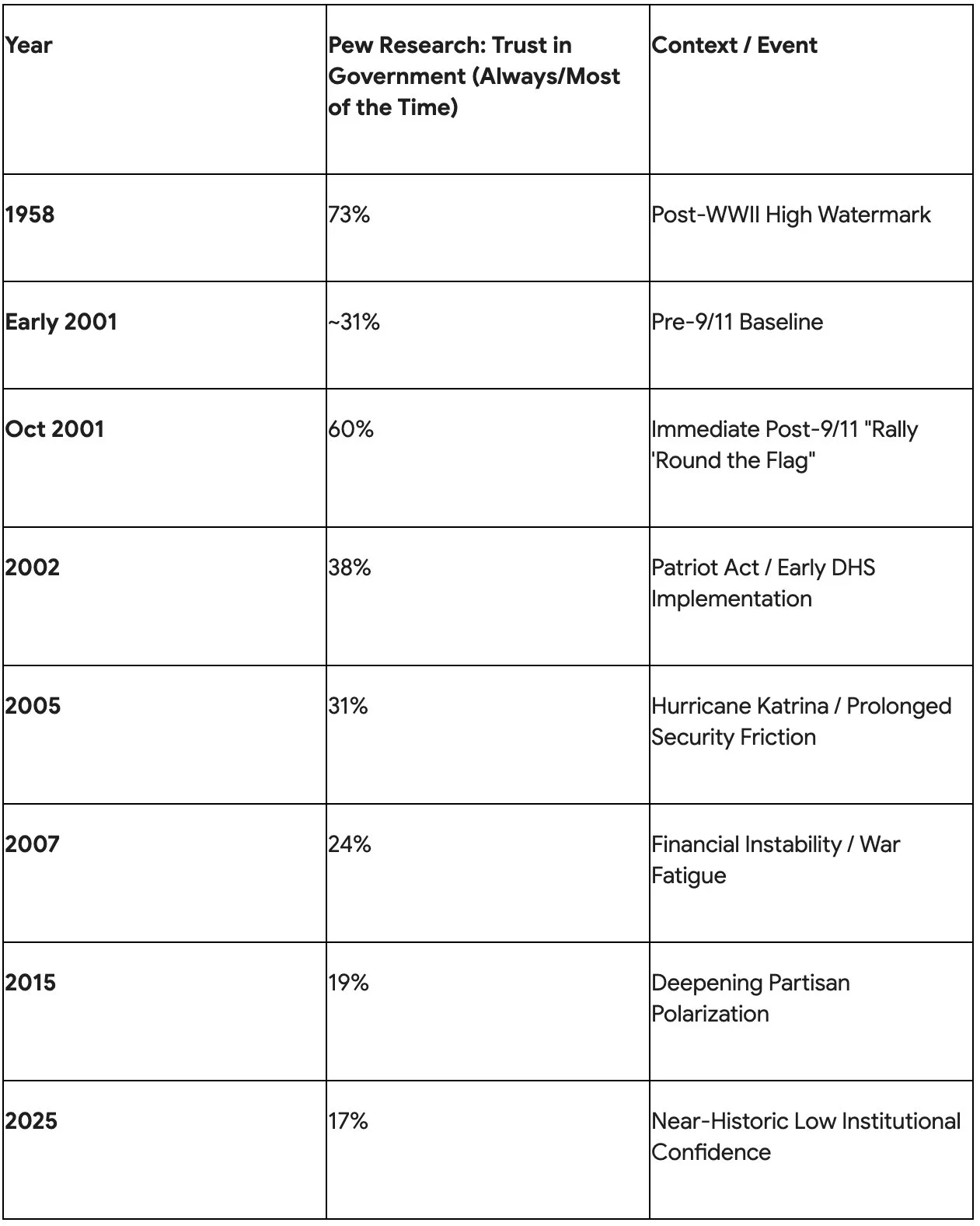

While the costly signaling initially stabilized the transition matrix, CBMT posits that the ultimate value of money relies on the long-term stability and health of the institutional social contract. Modern firms and economies are cooperative structures that rely on "Fitness Interdependence" or "Shared Fate" to minimize internal transaction costs. If the Leviathan's response to 9/11 was truly effective in the long run, we should observe a sustained high level of public trust in government institutions, reflecting a strong, organic Institutional Realization Rate ($IR$).

Longitudinal polling data from the Pew Research Center, Gallup, and the National Election Studies reveals a starkly different reality, suggesting a severe deterioration of the social contract.

Data compiled from.

In the immediate aftermath of the attacks, there was a profound psychological "rally 'round the flag" effect. In early October 2001, 60 percent of Americans expressed trust in the federal government—roughly double the share from earlier that year, marking the highest level of institutional trust in over four decades.

This spike, however, was highly fleeting. By the summer of 2002, the share of Americans trusting the government plummeted by 22 percentage points. Amid the implementation of the Patriot Act's surveillance authorities, the bureaucratic entanglements of the DHS, the war in Iraq, and ongoing domestic economic uncertainties, trust steadily eroded. By July 2007, trust had fallen to 24 percent. Decades later, by 2025, public trust in the federal government had decayed to a near-historic low of just 17 percent.

Specialized tracking of institutional confidence reveals that the DHS reorganization—moving 22 disparate agencies under a massive new umbrella reporting to Congress—resulted in a deeply dysfunctional, inflexible bureaucracy. Former TSA executives have openly referred to the agency as "hopelessly bureaucratic," with congressional reports blasting it for "costly, counterintuitive, and poorly executed" plans. The failure of the state to seamlessly restore order without infringing heavily on civil liberties, privacy, and economic efficiency paradoxically weakened the underlying social contract. In CBMT terms, while the state's costly signaling prevented the $IR$ from collapsing to zero in 2001, its heavy-handed, high-friction methodologies initiated a slow, multi-decade decay of the institutional coefficient.

CBMT Theoretical Predictions vs. Empirical Macroeconomic Reality

The ultimate test of any economic theory lies in its predictive validity. By applying the pure mechanics of Capacity-Based Monetary Theory to the 9/11 shock and the subsequent legislative friction, we can extrapolate a specific set of theoretical macroeconomic outcomes and compare them against the empirical data observed between 2000 and 2006. This discrepancy analysis reveals both the explanatory power and the crucial blind spots of the CBMT framework.

The Pure CBMT Theoretical Prediction

According to CBMT, money is a priced claim on Expected Future Impact. The events of 9/11 and the government response constituted a severe downward revision of this expected impact due to four intersecting factors:

Immediate, albeit localized, destruction of Physical Capital ($K$) and Human Capital ($H$).

A sudden, severe drop in the Institutional Realization Rate ($IR$) as transaction costs briefly approached the Hobbesian state.

A structural, permanent reduction in Efficiency ($A$) due to the deadweight loss of the ensuing security apparatus (Patriot Act AML costs, TSA travel friction).

A spike in the Hamilton Filter's probability of a "Collapse Regime," leading to a massive increase in the discount rate applied to the future.

Under strict CBMT mechanics, if realizable capacity ($Y_{realizable}$) degrades rapidly while the claim structure (the money supply) remains fixed or expands, the value of the currency must dilute rapidly. Therefore, CBMT would theoretically predict the following outcomes for the U.S. economy post-9/11:

High Inflation: As the "collateral" backing the currency shrinks relative to the money supply, the purchasing power of existing money drops.

Currency Depreciation: A collapse in the foreign exchange value of the U.S. dollar as international investors flee the degrading institutional social contract and rising transaction costs.

Spiking Real Interest Rates: Driven by a surging discount rate, as economic agents demand high risk premiums to hold claims on an uncertain future characterized by violence and institutional inefficiency.

The Real-World Empirical Data (2000–2006)

The empirical macroeconomic reality sharply diverged from the direst CBMT theoretical predictions. The U.S. macro-economy demonstrated profound resilience, absorbing the shock with surprising stability.

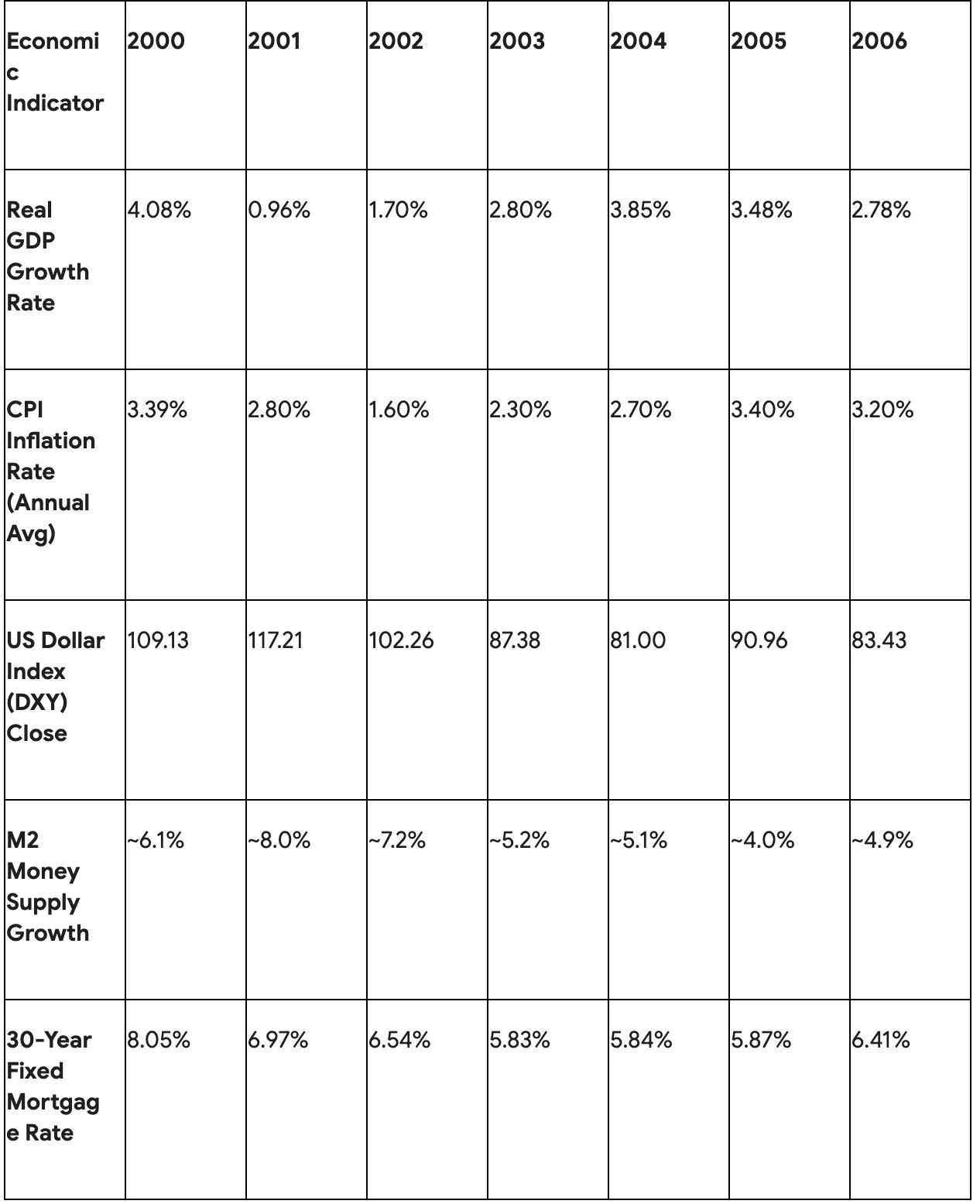

Data compiled from Federal Reserve Economic Data (FRED), Bureau of Labor Statistics, and Macrotrends historical datasets. Note: 30-Year Fixed Mortgage rates are used as a proxy for consumer-facing long-term interest rates.

1. GDP Resilience: While the U.S. economy was already in a contractionary phase prior to September 2001, real GDP growth slowed to 0.96% in 2001 but immediately rebounded to 1.70% in 2002 and 2.80% in 2003. The forecasted "jobless recovery" materialized early in 2002, but aggregate output recovered far faster than a "collapse regime" transition matrix would suggest.

2. Muted Inflation: Contrary to the CBMT prediction of rapid currency dilution resulting from degraded capacity, inflation actually fell in the immediate aftermath of the attacks. The CPI inflation rate dropped from 3.39% in 2000 to 2.80% in 2001, and further plummeted to 1.60% in 2002. It was not until 2005 that inflation returned to pre-9/11 levels (3.40%), largely driven by soaring energy prices rather than pure capacity degradation.

3. Dollar Strength: The U.S. Dollar did not experience an immediate run or depreciation. In fact, the DXY index closed significantly higher at the end of 2001 (117.21) than it did in 2000 (109.13). While the dollar did enter a multi-year depreciation trend thereafter—bottoming at 81.00 in 2004—the immediate reaction was one of aggressive currency strengthening, confounding standard capacity-dilution models.

4. Falling Real Interest Rates: Rather than spiking due to a surging discount rate and infinite transaction costs, nominal and real interest rates fell precipitously. A highly accommodative monetary policy engineered by the Federal Reserve lowered the target federal funds rate aggressively, keeping inflation pressures muted and credit spreads narrow. Average 30-year mortgage rates fell sequentially from 8.05% in 2000 to 5.83% by 2003.

Reconciling the Discrepancy: Hegemony, Liquidity, and the Solow Residual

The material differences between CBMT's pure theoretical predictions and the real-world macroeconomic facts expose necessary nuances, external variables, and missing dimensions in the base theory. Understanding why the U.S. economy defied the gravitational pull of capacity degradation requires examining three primary mitigating factors.

The Open-Economy Hegemon Exemption

CBMT, as articulated in its foundational text, primarily describes a closed institutional system where domestic capacity strictly dictates domestic currency value. However, the United States is the issuer of the global reserve currency. When the 9/11 shock occurred, the rest of the world did not view the event merely as an isolated degradation of U.S. capacity; they viewed it as a systemic global destabilization event.

Consequently, international capital engaged in a massive "flight to safety"—paradoxically rushing into U.S. Treasury securities and dollar-denominated assets. This immense exogenous demand for the dollar explains why the DXY index spiked to 117.21 in 2001, strengthening against a basket of foreign currencies despite the attacks on the U.S. homeland. The U.S. Leviathan benefits from a global institutional premium that buffers it against domestic $IR$ shocks. Because global trade and commodities are priced in dollars, the U.S. currency operates somewhat independently of immediate, localized capacity shocks, a reality that CBMT must incorporate to accurately model hegemonic fiat systems.

Monetary Accommodation and Velocity Collapse

CBMT accurately notes that if capacity ($Y$) drops, the value of the claim must dilute—if the supply of claims remains constant or grows. In the days and months following 9/11, the Federal Reserve took unprecedented action to flood the financial system with liquidity to prevent a deflationary spiral and maintain the clearing of checks and transactions. The M2 money supply growth rate surged, maintaining levels above 8.0% throughout the latter half of 2001.

In a standard quantity-theory framework, this massive injection of liquidity combined with a shock to capacity should have triggered immediate inflation. However, because the velocity of money collapsed—as consumers, businesses, and investors hoarded cash and shifted to highly liquid assets due to profound psychological uncertainty—the massive expansion of M2 simply offset the velocity shock. Thus, inflation fell to 1.6% in 2002. CBMT's intense focus on long-term capacity ($Y_{realizable}$) struggles to account for these short-term, central-bank-engineered liquidity bridges that effectively prevent the Hamilton Filter from locking the economy into a terminal "Collapse Regime."

The Solow Residual Boom: Masking Regulatory Deadweight Loss

Finally, CBMT assumes a somewhat rigid relationship between institutional friction, transaction costs, and overall capacity realization. While the DHS and the Patriot Act undoubtedly introduced severe deadweight losses and degraded efficiency, the U.S. economy demonstrated extraordinary underlying adaptability.

During the latter half of the 1990s and continuing robustly through the early 2000s, labor productivity (defined as output per hour) in the nonfarm business sector surged. From 2000 to 2007, productivity growth averaged between 0 and 4 percent per year across most industries, heavily driven by the integration of information technology (IT), advanced software, and wireless telecommunications.

This underlying boom in the efficiency variable ($A$) and the Solow Residual effectively masked the deadweight loss imposed by the homeland security regulations. The technological amplification of labor and the optimization of supply chains were so potent that they vastly outpaced the frictional drag of TSA screening lines, Patriot Act AML compliance costs, and border delays. The U.S. economy grew despite the imposition of the new security state, not because of it. The technological expansion of the production function absorbed the shock, allowing the Leviathan to impose trillions of dollars in security costs without immediately plunging the nation into a stagflationary crisis.

Synthesis and Conclusion: The Long-Term Institutional Legacy

Applying Capacity-Based Monetary Theory to the events of September 11, 2001, provides a deeply illuminating framework for understanding the ontological shift in the American economy over the past two decades. While traditional economic analysis successfully measures the physical destruction of the day and the immediate fiscal outlays, CBMT forces the analyst to rigorously measure the destruction of institutional efficiency and the manipulation of the social contract.

The legislative response to 9/11—most prominently the USA PATRIOT Act and the establishment of the Department of Homeland Security—was an aggressive, highly rational attempt by the Leviathan to restore the Institutional Realization Rate ($IR$) and prevent a permanent regime shift in the macroeconomic Hamilton Filter. By utilizing Zahavi's Handicap Principle, the state burned massive amounts of capital to signal its enduring strength to the global market.

However, an analysis of the effectiveness of this legislation reveals profound structural failures and hidden taxes. The imposition of over \$1 trillion in domestic security costs, the creation of regressive, wealth-redistributing compliance burdens on the banking sector, and the permanent frictional drag on global travel and trade represent severe, enduring deadweight losses. These interventions failed basic cost-benefit analyses by orders of magnitude and ultimately resulted in a steady, two-decade erosion of public trust in government, undermining the very Shared Fate and Fitness Interdependence required to maintain a high-capacity civilization.

Yet, a meticulous discrepancy analysis reveals that CBMT's direst theoretical predictions of hyperinflation, spiking interest rates, and immediate currency collapse did not materialize. The U.S. economy was buffered not by its newly erected security apparatus, but by the exogenous demand for the dollar as a global reserve asset, masterful short-term liquidity interventions by the Federal Reserve, and a historic, underlying boom in technological productivity that vastly outpaced the government's newly imposed transaction costs.

Ultimately, the events of 9/11 and the subsequent legislative responses fundamentally and permanently altered the production function of the United States. The nation transitioned into a state of permanently elevated institutional friction. By viewing money not just as a medium of exchange, but as a dynamically priced claim on future impact, it becomes evident that the true, lasting cost of the post-9/11 security apparatus was not just the physical capital expended, but the vast expanse of future human capacity that was restricted, diverted, and never fully realized.