How can California Build Back Better?

The California Commerce Capacity Network: A State-Led Blueprint for Main Street Economic Development and Public Banking

The contemporary digital payments landscape presents a profound structural disadvantage for small and medium-sized enterprises (SMEs), bifurcating the modern economy into two distinct financial realities. On one side of the market, global open-loop credit networks, dominated by a duopoly of massive financial institutions, facilitate universal exchange but extract severe economic rents. These networks typically siphon 2% to 3% of the total transaction value in the form of interchange and swipe fees, creating an enormous drag on the profitability of independent businesses. On the other side of this divide exist proprietary closed-loop systems, most prominently exemplified by the Starbucks mobile application. These highly centralized, corporate-owned networks offer a seamless user experience, incur zero transaction fees for the issuer, and allow the corporate entity to monetize a massive pool of prepaid customer funds. This aggregated capital—a "float" which in Starbucks' case exceeds $1.6 billion—functions as an interest-free loan from the consumer base, which the corporation can aggressively reinvest into its own operational capacity.

Historically, regulatory frameworks such as the federal Bank Secrecy Act (BSA) and a labyrinth of state-level money transmission laws have structurally prevented independent, unaffiliated businesses from federating to replicate this highly efficient closed-loop model. As a result, independent Main Street merchants are relegated to the punitive costs of the open-loop market, unable to harness the float economics enjoyed by multinational conglomerates. However, the State of California possesses the unique jurisdictional authority, capital scale, and existing institutional infrastructure to bridge this divide.

By adapting the private-sector "Federated Capacity Network" business model into a state-run public utility, California can architect a revolutionary economic engine: The California Commerce Capacity Network (C3N). Rather than relying on a private corporation to manage this network, the State of California can act as the central federator. Operating through existing agencies such as the Infrastructure and Economic Development Bank (IBank) and the Governor's Office of Business and Economic Development (GO-Biz), the state can provide California-based SMEs with zero-fee transaction processing. Simultaneously, the platform will aggregate the localized consumer float into a newly established California Sovereign Wealth Fund. This fund will, in turn, provide low-cost, capacity-building working capital loans directly to the participating merchants, effectively turning consumer purchasing power into a perpetual engine for local economic development.

Executing this state-led paradigm shift requires navigating a complex matrix of economic theory, statutory exemptions, constitutional law, and enterprise-grade technology. This report provides an exhaustive analysis of the architecture required to realize the C3N, detailing how the state can navigate the Money Transmission Act, overcome constitutional restrictions regarding the gift of public funds, deploy advanced PostgreSQL and Fireblocks technical stacks, and ultimately frame the initiative as a highly resonant, voter-friendly political campaign against financial monopolies.

1. Theoretical Foundations: Public Capacity-Based Monetary Theory (CBMT)

To construct a state-run payment utility that can withstand systemic market volatility and regulatory scrutiny, the operational model must be grounded in a rigorous, forward-looking economic ontology. The C3N discards the traditional neoclassical view of prepaid digital tokens as mere financial liabilities or passive "stores of value." Instead, the platform's economics operate on Capacity-Based Monetary Theory (CBMT), which posits that a prepaid credit is fundamentally a floating-price claim on the future productive capacity of a specific economic network.

1.1 The State Token as a Derivative of Future Impact

Under standard Generally Accepted Accounting Principles (GAAP), when a California consumer converts fiat currency into a digital C3N credit, the transaction is recorded as a liability ("Deferred Revenue") balanced by a cash asset in the state treasury. However, CBMT dictates that the true asset backing this sovereign system is not the fiat cash sitting dormant in a bank, but rather the Expected Future Impact ($E_{FI}$) of the Californian SME network.

When a consumer purchases a digital token on the C3N platform, they are essentially acquiring a call option on the Real Output ($Y$) of local, vetted merchants. They are placing an economic bet that, at the time of redemption, the local merchant network will possess the aggregate labor, physical capital, and human capital required to honor that claim with goods or services. Therefore, the fundamental value of the state network's credit ($V_{token}$) is not derived from fiat reserves alone, but functions as a direct index of the participating merchants' aggregated production function.

To quantify this capacity at a macroeconomic, state-wide level, the C3N utilizes the Augmented Solow-Swan model, as specified by economists Mankiw, Romer, and Weil :

$$Y(t) = A(t) \cdot K(t)^\alpha \cdot H(t)^\beta \cdot L(t)^{1-\alpha-\beta}$$

Within the context of the California Commerce Capacity Network, the variables are defined as follows:

- $Y(t)$ (Impact): The aggregate goods, services, and innovations available for redemption within the California independent merchant network.

- $A(t)$ (Efficiency Capacity): The labor-augmenting, friction-reducing technology of the C3N platform. This is primarily driven by the elimination of the 3% open-loop interchange fees and the implementation of high-speed PostgreSQL settlement, which dramatically lowers the cost of doing business.

- $K(t)$ (Physical Capital): The tangible assets of California's independent merchants, such as retail space, commercial ovens, inventory, and point-of-sale systems. Crucially, this variable is financed directly by the state's sovereign wealth float.

- $H(t)$ (Human Capital): The localized workforce skill, education, and service quality. CBMT emphasizes that this is an independent factor of production with its own accumulation dynamics, which the state can foster through targeted technical assistance programs.

- $L(t)$ (Labor): The aggregate workforce of the participating SMEs.

The strategic implication of this theoretical framework is profound. The State of California is no longer merely functioning as a passive payment processor moving integers between databases; it is acting as a sovereign underwriter of state economic capacity. If the aggregate physical capital ($K$) or human capital ($H$) of the local economy degrades—if merchants lose skilled staff or cannot afford to repair failing equipment—the intrinsic "collateral" backing the state token erodes, leading to a collapse in the network's utility. Therefore, the state must actively manage the aggregated float, aggressively reinvesting it back into the network to elevate the production function rather than allowing it to sit passively in traditional, low-yield securities.

1.2 The Institutional Realization Rate ($\gamma$) and State Backing

Theoretical capacity remains purely theoretical until it is reliably delivered to the consumer. CBMT introduces the concept of the Institutional Realization Rate ($\gamma$), a coefficient between 0 and 1 that quantifies the frictional costs of trust, order, and contract enforcement within the economic system.

$$V_{claim} = E_{FI} \cdot \gamma$$

In a centralized, proprietary model like Starbucks, $\gamma$ approaches 1 because a single, highly capitalized corporate entity controls both the issuance of the token and its redemption. The "social contract" of the transaction is enforced by absolute corporate fiat. However, for a decentralized network composed of thousands of unaffiliated independent merchants, $\gamma$ represents the primary vulnerability. If a local merchant experiences a technical failure, or simply refuses to accept the state digital credit, the perceived value of the system deteriorates rapidly in the eyes of the consumer, regardless of the theoretical capacity of the broader network.

By operating the platform as a trusted state utility, and by algorithmicizing the institutional social contract via immutable digital ledgers and strict technical onboarding requirements, the State of California can artificially elevate $\gamma$ to levels that are competitive with multinational monopolies. The state's inherent authority and regulatory oversight provide the ultimate guarantee of trust, ensuring that consumer confidence in the state-backed digital credit remains absolute.

2. Navigating the Regulatory Labyrinth: The Legal Architecture

The principal barrier to establishing a shared, zero-fee payment network for independent businesses is the dense thicket of state and federal financial regulations designed to prevent money laundering and ensure consumer protection. Adapting the private Federated Capacity Network into a public utility requires a precise, nuanced application of the California Financial Code and the California Constitution.

2.1 The FinCEN "Affiliated Group" Trap and the Money Transmission Act

Under federal regulations administered by the Financial Crimes Enforcement Network (FinCEN), specifically the Prepaid Access Rule (31 C.F.R. § 1010.100(ff)), an arrangement where funds are paid in advance and retrievable via an electronic device is heavily regulated. Entities providing these programs are classified as Money Services Businesses (MSBs), which triggers exhaustive requirements for federal registration, comprehensive Anti-Money Laundering and Know Your Customer (AML/KYC) compliance programs, and the continuous filing of Suspicious Activity Reports (SARs).

FinCEN does provide an exemption for "closed-loop prepaid access" where the funds are limited and can only be used at a "single merchant or an affiliated group of merchants". However, FinCEN and the Consumer Financial Protection Bureau (CFPB) define an "affiliated group" extremely narrowly, requiring the merchants to be related by common ownership or common corporate control (e.g., franchisees operating under a single corporate umbrella). Consequently, a network of independent, unaffiliated Main Street businesses attempting to share a unified payment application falls squarely into the heavily regulated "open-loop" or "Restricted Access Network" (RAN) categories.

At the state level, the California Money Transmission Act (MTA), enacted via AB 2789, broadly defines "money transmission" to include the selling or issuing of stored value instruments and the receiving of money for transmission. Operating without navigating these statutes would subject the C3N to untenable compliance friction. To operationalize the C3N without suffocating under MSB requirements, the state must rely on two distinct and highly effective statutory exemptions found within California Financial Code Section 2010.

2.2 The Governmental Agency Exemption (Financial Code § 2010(c))

The most direct shield against the MTA is the inherent nature of the platform's operator. California Financial Code Section 2010 expressly outlines entities to which the division does not apply. Section 2010(c) explicitly exempts: "A state, county, city, or any other governmental agency or governmental subdivision of a state".

By housing the C3N directly within a recognized state agency—such as the State Treasurer's Office or the Governor's Office of Business and Economic Development (GO-Biz)—the platform inherently bypasses the jurisdiction and licensing requirements of the MTA. This mirrors the regulatory strategy developed for the CalAccount Blue Ribbon Commission (AB 1177), which seeks to establish state-backed transaction accounts free from traditional banking fees by utilizing the state's sovereign standing.

2.3 Master Agent of the Payee Exemption (Financial Code § 2010(l))

While the governmental exemption protects the state operator, providing commercial clarity and risk mitigation for the private merchants requires a second layer of legal structuring: the "Agent of the Payee" exemption.

California Financial Code Section 2010(l) exempts from the MTA any transaction "in which the recipient of the money or other monetary value is an agent of the payee pursuant to a preexisting written contract and delivery of the money or other monetary value to the agent satisfies the payor's obligation to the payee".

Operationally, this is the linchpin of the C3N network:

- Contractual Agency: The State of California enters into a formalized commercial agreement with every participating SME (the Payee). This contract explicitly appoints the state agency as the merchant's authorized agent solely for the receipt of payments.

- Extinguishment of Debt: The Terms of Service (TOS) dictate a "constructive receipt" clause. The exact millisecond a consumer (the Payor) transfers funds into the state's C3N ledger, the consumer's payment obligation to the merchant is legally extinguished.

- Risk Transfer: Because the state acts as the master agent, the state is not transmitting money for the consumer; it is collecting money on behalf of the merchant. The merchant bears the credit risk of the state platform, not the consumer. This fully satisfies the policy goals of money transmission regulations, which are designed to protect consumers from intermediary insolvency.

Recent regulatory actions by the California Department of Financial Protection and Innovation (DFPI) heavily support this architecture. Through numerous opinion letters and rulemakings, the DFPI has affirmed that platforms intermediating payments—such as online marketplaces and payment processors—are exempt from MTA licensure so long as the contractual language explicitly establishes this agency relationship and debt extinguishment. By embedding this language into the foundational architecture of the C3N, the state guarantees a compliant, frictionless environment for the aggregation of localized capital.

Legal Exemption Strategy Statutory Authority Operational Application for C3N Regulatory Benefit Governmental Agency Cal. Fin. Code § 2010(c) Network operated by GO-Biz / State Treasurer Exempts platform operator from MTA licensure Agent of the Payee Cal. Fin. Code § 2010(l) State acts as authorized collection agent for SMEs Extinguishes consumer debt instantly upon payment Closed-Loop Safe Harbor 31 C.F.R. § 1010.100(ff) Transaction limits capped at $2,000 per day Avoids federal FinCEN MSB classification

3. Overcoming Constitutional Barriers: The Gift of Public Funds Doctrine

Because the aggregated consumer float will be actively utilized to provide capacity-building loans to participating private businesses, the state must carefully navigate Article XVI, Section 6 of the California Constitution. This section strictly prohibits the legislature or any public agency from making a "gift of public funds" or lending its public credit to any private individual, association, or corporation.

Historically, this provision was enshrined to prevent the state treasury from subsidizing private enterprises, which poses a prima facie threat to a state-run merchant loan program funded by a centralized float. However, California jurisprudence has established a robust and highly flexible "Public Purpose" exception.

3.1 The Public Purpose Exception

As articulated by the California Supreme Court in the landmark case County of Alameda v. Janssen (1940), and repeatedly affirmed in subsequent rulings such as Redevelopment Agency of San Pablo v. Shepard (1977), the primary question in determining the constitutionality of an appropriation is the ultimate destination of the benefit. The Court noted: "If they are for a 'public purpose', they are not a gift within the meaning of. The benefit to the state from an expenditure for a 'public purpose' is in the nature of consideration and the funds expended are therefore not a gift even though private persons are benefited therefrom".

In essence, if the primary objective of the financial program serves a broader public interest, the fact that private entities (such as independent coffee shops or retail stores) receive an incidental financial benefit or loan does not render the transaction unconstitutional.

3.2 Structuring the Legislative Mandate

To permanently immunize the C3N lending mechanisms from constitutional challenges, the enabling legislation must feature explicit, meticulously drafted legislative findings declaring the program's public purpose. Courts generally exercise extreme deference to legislative determinations of public purpose, provided those determinations have a reasonable basis.

The statutory text establishing the C3N must codify that providing immediate liquidity and zero-fee payment infrastructure to California SMEs is not a corporate subsidy, but a vital public mechanism. The legislation must assert that the network:

- Secures the financial condition of community economies that are disproportionately harmed by macroeconomic volatility.

- Prevents commercial blight and neighborhood decay by ensuring local businesses remain solvent.

- Democratizes access to capital for underbanked entrepreneurs, thereby advancing the state's goals of economic equity and job retention.

By framing the capacity-based loans as the direct "consideration" the state pays to maintain a thriving, tax-generating Main Street economy, the C3N satisfies the constitutional requirements and clears the path for aggressive financial deployment.

4. The California Sovereign Wealth Engine: Float Management

The aggregation of millions of consumer prepaid transactions creates a massive, highly liquid "float." In the private sector model, this float represents the primary economic engine of the payment platform. For the state, this capital will be pooled into a newly conceptualized sovereign wealth vehicle, representing a major evolution in public finance.

Historically, proposals for state sovereign funds or public banking entities—such as the "California Investment Trust" proposed under AB 750 and AB 2500—aimed to utilize state tax deposits for commercial lending and infrastructure. Similarly, the landmark California Public Banking Act (AB 857), signed into law in 2019, empowered local municipalities to form public banks specifically to redirect municipal tax dollars away from Wall Street. The C3N advances these concepts by generating its capital base not through the taxation of residents, but through the voluntary, circulating consumer float of the retail economy.

(Strategic Note on Nomenclature: Care must be taken in legislative drafting to distance this fund from the name "California Future Fund." That specific moniker is deeply tainted in California political history due to its association with a 2012 dark-money political action committee that was heavily penalized by the FPPC and the Attorney General for campaign finance violations and laundering out-of-state money to oppose tax initiatives. The new entity should maintain a distinct, purely economic nomenclature, such as the "California Capacity Trust" or the "Main Street Reinvestment Fund.")

4.1 Resolving the Investment Company Act Friction

For private fintech companies, aggregating a multi-million dollar float and issuing loans poses a severe existential risk of being classified as an "Investment Company" by the SEC under the Investment Company Act of 1940 ("the '40 Act"). The '40 Act mandates that if "investment securities" comprise more than 40% of an issuer's total assets, the entity is subject to draconian registration, capitalization, and operational restrictions that are structurally incompatible with running a high-velocity payment business.

While state-operated instrumentalities are broadly exempt from federal '40 Act registration, the underlying economic principles of asset-liability matching and systemic risk mitigation remain an imperative fiduciary duty for the state. To optimize yield and ensure the Institutional Realization Rate ($\gamma$) never fractures due to a sudden liquidity crisis (a "bank run" on the platform), the state sovereign fund must deploy a rigorous "Capacity Reinvestment Strategy" tailored to balance economic stimulation with absolute solvency.

4.2 The Tiered Capacity Reinvestment Portfolio

The float management protocol dictates that capital be apportioned strictly according to asset liquidity profiles and network capacity requirements:

Tier 1: The Liquidity Buffer (40% Allocation)

- Composition: Demand deposits, state treasury sweep accounts, and direct holdings of highly liquid short-term U.S. Treasury Bills.

- Purpose: Ensures immediate, high-velocity settlement capability. This absolute buffer guarantees that participating merchants are paid out on a T+0 or T+1 schedule, regardless of broader macroeconomic liquidity conditions, thereby bulletproofing the network's $\gamma$ coefficient.

- Integration: These funds can be efficiently managed through existing state infrastructure, such as the Local Agency Investment Fund (LAIF), a highly successful California state investment pool available to public entities.

Tier 2: Merchant Capacity Loans (40% Allocation)

- Composition: Direct short-term working capital loans, inventory financing, and equipment leases extended exclusively to the participating California SMEs within the network.

- Purpose: This tier represents the operationalization of Capacity-Based Monetary Theory. By lending the aggregated float back to the very merchants that constitute the network to acquire physical capital ($K$) and human capital ($H$), the state artificially and deliberately increases the economic collateral backing its own digital token.

- Risk Mitigation: Default risk is virtually eliminated through the Master Agent of the Payee structure. Because the state controls the payment settlement ledger natively, daily loan repayments are programmatically deducted from the merchant's gross daily transaction inflows. This mimics a zero-friction Merchant Cash Advance (MCA) model, making underwriting highly reliable and recovery automatic.

Tier 3: Infrastructure and Public Yield (20% Allocation)

- Composition: Longer-term state infrastructure bonds, municipal debt instruments, or carefully vetted, compliant digital yield products.

- Purpose: Reinvesting the remaining, highly stable portion of the float into state-backed public works or climate infrastructure. This ensures that the economic momentum generated by the retail sector directly finances civic improvements, deeply aligning with the objectives of the California Infrastructure and Economic Development Bank.

4.3 Dynamic Risk Management via AI and Hamilton Filters

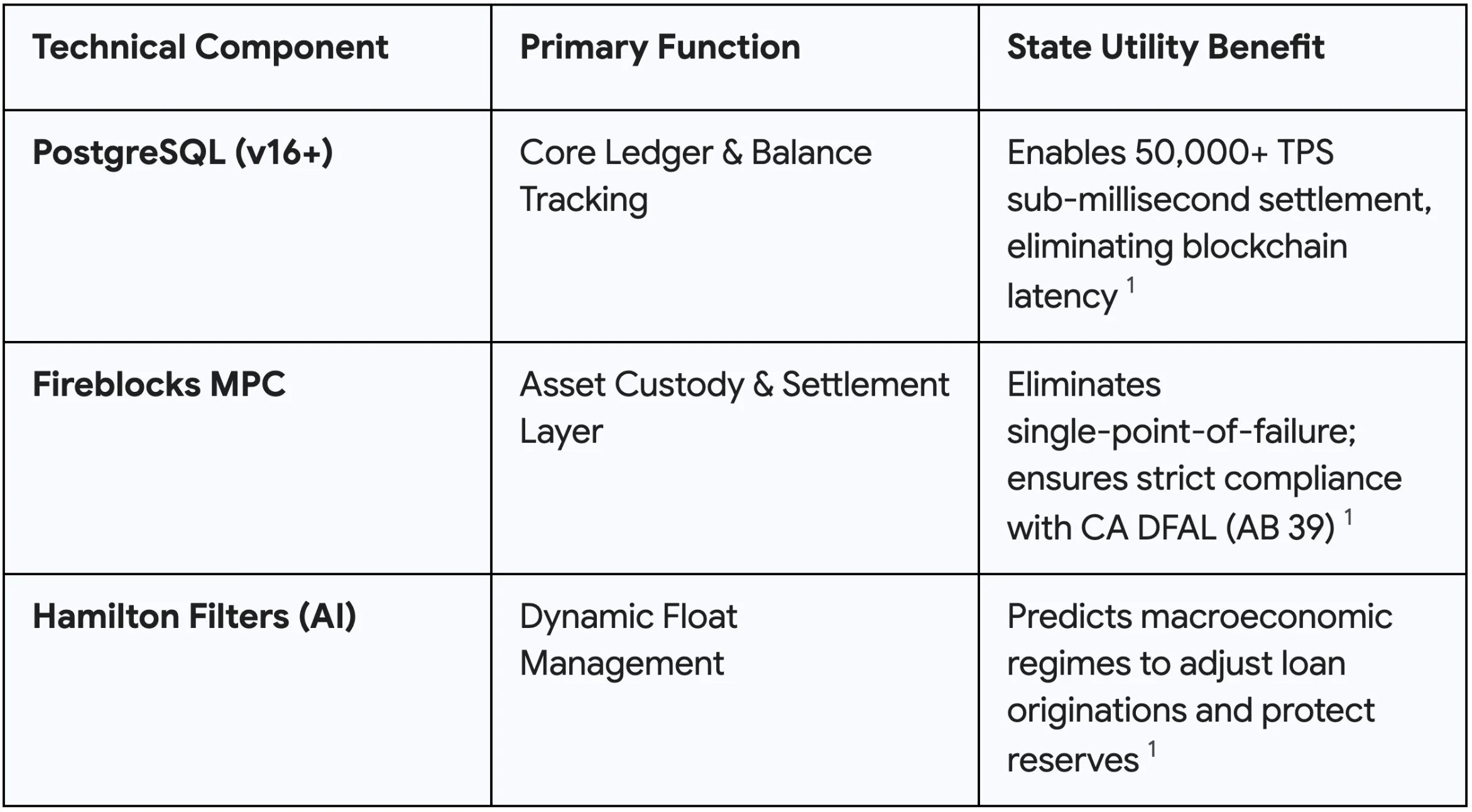

The macroeconomy is not static; it constantly shifts between distinct economic "regimes" (e.g., periods of rapid expansion versus periods of recessionary contraction or high inflation). To oversee the systemic risk of the float and protect the state's liability, the C3N will deploy sophisticated Artificial Intelligence models utilizing Hamilton Regime-Switching Filters.

The AI model actively analyzes multi-dimensional time-series data—including California inflation rates, local unemployment figures, C3N token redemption velocity, and merchant chargeback volumes. Using this data, the Hamilton Filter algorithms estimate the probability ($P$) of the state economy occupying a specific regime at any given moment.

During a detected "Stable Growth" regime, the AI authorizes the expansion of Tier 2 capacity loans, maximizing economic stimulus and yield while future impact is expected to be abundant. Conversely, if the filter detects a shift toward a "Volatility/Crisis" regime—indicating a higher probability of consumer hoarding, degrading capacity, or a "run" on token redemptions—the AI policy engine automatically triggers a defensive posture. It restricts new Tier 2 loan originations, halts Tier 3 allocations, and rebalances the portfolio to maximize Tier 1 cash reserves. This algorithmic foresight hardens the system against economic shocks, guaranteeing that the state can always honor its capacity claims without requiring a taxpayer bailout.

5. Institutional Integration: Leveraging IBank, GO-Biz, and CalAccount

The realization of the California Commerce Capacity Network does not require the creation of a massive, redundant bureaucracy from scratch. California already possesses a mature, highly capable ecosystem of economic development agencies capable of absorbing, operating, and scaling this platform.

5.1 Governor's Office of Business and Economic Development (GO-Biz)

GO-Biz serves as the state's apex entity for job growth, corporate retention, and overall economic strategy. Within the GO-Biz umbrella, the California Office of the Small Business Advocate (CalOSBA) provides critical operational support, serving as the official voice and resource hub for the state's 4.1 million small businesses.

CalOSBA's existing, extensive network of Small Business Development Centers (SBDCs) and technical assistance programs will serve as the primary onboarding and vetting conduit for the C3N. To ensure the integrity and quality of the merchant network, the state will implement the "Handicap Principle" derived from economic Signaling Theory. Rather than relying on superficial, easily manipulated credit checks, the C3N will mandate full API integration with the merchant's Point-of-Sale (POS) system as a prerequisite for joining.

This technological friction serves as a "costly signal" that effectively filters out transient, low-quality, or fraudulent operators ("lemons"). Only technologically competent and committed merchants, who expect to remain in business long enough to amortize the cost of integration, will undertake the effort. CalOSBA will play a vital role here, providing the targeted technical assistance and resources required to help legitimate but under-resourced minority and rural merchants achieve this integration, ensuring equitable access to the network.

5.2 California Infrastructure and Economic Development Bank (IBank)

IBank, housed within GO-Biz, is the state's premier financial assistance and infrastructure lending apparatus. IBank's Small Business Finance Center (SBFC) currently administers highly successful programs such as the Small Business Loan Guarantee Program (SBLGP) and processes massive allocations from the federal State Small Business Credit Initiative (SSBCI), which recently provided California with over $1.2 billion in funding to enhance capital access.

The C3N's Tier 2 capacity loans will be seamlessly integrated into the SBFC's operational matrix. By utilizing the federal SSBCI funds as a primary risk backstop, and incorporating IBank's established relationships with mission-driven Community Development Financial Institutions (CDFIs) and Financial Development Corporations (FDCs), the state can rapidly deploy the C3N float. This structure allows the state to underwrite loans to businesses that traditionally fail to meet the rigid, risk-averse underwriting standards of massive commercial banks, heavily accelerating local economic mobility.

5.3 Consumer Synergy with CalAccount (AB 1177 / AB 1365)

While the C3N architecture fundamentally addresses the merchant-side of the economic equation, it achieves maximum velocity and societal impact when paired with the consumer-side infrastructure of the CalAccount program.

Established by the Public Banking Option Act (AB 1177) and refined through subsequent legislation (AB 1365), CalAccount is designed to provide free, universal financial services to the millions of unbanked and underbanked Californians through a voluntary, zero-fee, zero-penalty debit account managed by the state. Following exhaustive market analyses and feasibility studies conducted by the Blue Ribbon Commission and the RAND Corporation, CalAccount is poised to close the gaps left by traditional, predatory banking.

By directly linking the CalAccount consumer ledgers with the C3N merchant platform, the state creates an entirely frictionless, localized, end-to-end digital economy. Low-income residents can utilize CalAccount to securely hold their wages without facing overdraft fees, and then spend those funds directly at local SMEs via the C3N network. This perfectly contained ecosystem bypasses the extractive toll bridge of corporate payment processors entirely, ensuring that 100% of the transactional wealth remains circulating within the California economy, rather than being siphoned off to Wall Street.

6. Technical Infrastructure: The Digital Public Utility

To support the demands of an economy the size of California's—processing millions of daily micro-transactions—the C3N requires an enterprise-grade, highly scalable technological foundation. While decentralized, public blockchain frameworks dominate modern fintech discourse, the state requires absolute centralized authority, sub-millisecond latency, and rigid regulatory compliance, rendering pure public blockchain architectures highly inefficient and legally perilous.

6.1 The Core Ledger: PostgreSQL

The primary ledger—serving as the absolute, indisputable source of truth for consumer balances, merchant settlements, and Tier 2 loan repayments—will be built on advanced relational database architecture, specifically PostgreSQL (v16+).

Unlike public blockchains, which suffer from severe latency bottlenecks and low throughput (often limited to 300-500 transactions per second with extended block times), PostgreSQL can process upwards of 50,000+ TPS on standard hardware. For a state-run "closed-loop" network attempting to displace Visa and Mastercard at the point of sale, sub-millisecond latency is non-negotiable. Auditability, security, and transparency—the traits typically sought from blockchain—are instead maintained through immutable, append-only log tables built directly into the SQL architecture, avoiding the heavy computational and maintenance overhead of a decentralized ledger.

6.2 Institutional Custody and DFAL Compliance: Fireblocks

While the internal sub-ledger balances are tracked with extreme speed via PostgreSQL, the underlying settlement layer handling the actual digitized fiat reserves, or institutional stablecoins utilized in Tier 3 yield generation, requires military-grade security. For this, the C3N will utilize Fireblocks Multi-Party Computation (MPC) infrastructure.

MPC technology splits private cryptographic keys into multiple disparate shares, entirely eliminating the single points of failure that plague standard digital asset custody solutions. This architecture allows the state to programmatically whitelist approved merchant wallets, cryptographically enforcing the "closed-loop" restrictions required to maintain the legal exemptions under the Money Transmission Act.

Furthermore, utilizing Fireblocks ensures the state operations align with the stringent cybersecurity and operational benchmarks demanded by the recently enacted California Digital Financial Assets Law (DFAL, AB 39). DFAL imposes strict licensing, capital, and monthly reporting requirements on digital asset custody and exchange activities operating within the state. Implementing NIST-aligned Fireblocks custody guarantees the state's sovereign wealth engine operates with unassailable technical integrity.

6.3 Advanced AI Implementations: Security and Support

Beyond the Hamilton Filters managing the float, the state will deploy Artificial Intelligence to optimize operations and aggressively secure the network:

- Structuring and Fraud Detection: The state will utilize unsupervised machine learning algorithms, specifically Scikit-learn Isolation Forests, to identify multidimensional anomalies in transaction data. This is an essential tool for detecting "Structuring" or "Smurfing"—a technique where illicit actors break down large transactions into smaller increments (e.g., multiple \$1,900 transactions) specifically to evade the \$2,000 reporting thresholds mandated by FinCEN.

- Constituent and Merchant Support: The network will deploy Retrieval-Augmented Generation (RAG) language models for highly responsive customer service. Crucially, these models will be grounded securely in a state-controlled vector database containing only specific C3N policies, Terms of Service, and MTA guidelines. This architecture ensures that automated support provides hyper-accurate, legally compliant answers, entirely neutralizing the hallucination risks associated with raw, unconstrained Large Language Models (LLMs) that could inadvertently violate the network's closed-loop legal status.

7. Political Strategy: Taking it to the Voters

A structural economic reform of this magnitude will face immediate, heavily funded opposition from incumbent financial monopolies. Corporate payment networks (Visa, Mastercard) and massive commercial retail banks inherently profit from the extractive friction of the current system and will aggressively combat any state-led initiative that threatens their margins. Historically, the commercial banking lobby has fiercely opposed public banking initiatives in California, arguing through political action committees that public banks present undue risk to taxpayer funds and distort the free market.

To circumvent the inevitable legislative gridlock induced by financial lobbying, the creation of the C3N may be most effectively pursued via the California ballot initiative process. This constitutional mechanism allows citizens to bypass the legislature and directly amend state statutes. Winning at the ballot box, however, requires distilling the highly technical mechanics of CBMT, database architecture, and the Money Transmission Act into clear, resonant, populist messaging that motivates millions of voters.

7.1 The Core Narrative: "Main Street vs. Wall Street"

The initiative campaign must be aggressively anchored in the enduring populist dichotomy of "Main Street vs. Wall Street". The narrative presented to the voter is straightforward and highly relatable: multinational banks and corporate credit networks act as an unavoidable tollbooth on the California economy, draining billions of dollars annually from local neighborhood shops through hidden swipe fees.

By defining the 3% interchange fee not as a service cost, but as an extractive, regressive tax levied on small businesses by out-of-state monopolies, the C3N is presented not as a complex financial mechanism, but as a vital public utility designed to liberate local entrepreneurs. Polling data consistently demonstrates that while voters remain deeply wary of Wall Street institutions (with significant majorities believing big bankers often act deceptively and prioritize profits over consumer welfare), they are highly supportive of initiatives that foster local economic resilience and small business success.

7.2 Synergy with the "Honest Pricing" Movement

The messaging strategy will heavily leverage the massive political momentum generated by recent California consumer protection legislation, particularly SB 478 (commonly known as the "Honest Pricing Law" or "Hidden Fees Statute"). SB 478, which enjoyed broad public support, banned deceptive "drip pricing" and hidden junk fees across the retail, event, and hospitality spectrums, forcing corporations to display the true cost of goods.

The C3N campaign will co-opt this highly successful framework, arguing that the ultimate "hidden fee" in the modern economy is the credit card swipe fee silently inflating the cost of every single consumer good in the state. By framing the establishment of a zero-fee state payment network as the next logical, necessary step in the fight for price transparency and cost-of-living affordability, the initiative aligns perfectly with peak voter demand for economic relief.

7.3 Empowering Communities Over Monopolies

Opponents, funded by the banking lobby, will undoubtedly run negative ad campaigns arguing that state-run financial systems are prone to corruption, mismanagement, and taxpayer bailouts, echoing the precise criticisms leveled during the intense debates over the California Public Banking Act (AB 857).

The counter-narrative must preemptively emphasize that the C3N is mathematically governed. The campaign will highlight that the sovereign float is managed by transparent algorithms (the AI Hamilton Filters) and overseen by the established, highly respected fiduciary infrastructure of the State Treasurer, IBank, and CalOSBA, rigorously mitigating any risk of political favoritism or human error.

Furthermore, the campaign will tap into the state's progressive energy surrounding economic democratization. Just as advocates have successfully pushed to curtail the political influence of billionaires and dark money—evidenced by recent laws banning election sweepstakes and historic crackdowns on opaque entities like the "California Future Fund"—the C3N represents structural democratization. It shifts immense financial power away from centralized banking oligopolies and distributes it directly back to the localized, productive economy.

7.4 Asymmetric Grassroots Mobilization

To counter the massive campaign war chests that the financial industry will deploy, the initiative will rely on highly organized, asymmetric grassroots mobilization. This includes extensive, volunteer-driven text banking, phone banking, and letter-writing campaigns, utilizing platforms that empower citizens to spark chain reactions of civic engagement directly from their smartphones.

By forging strategic partnerships with small business coalitions, the California Democratic Party, labor unions, and local public banking alliances, the campaign will distribute promotional toolkits directly to small business owners. This strategy turns thousands of local storefronts across the state into organic advocacy hubs, transforming the businesses that will benefit most from the C3N into the primary messengers of the campaign, establishing deep trust with the voting public.

Strategic Synthesis and Conclusion

The California Commerce Capacity Network represents a monumental paradigm shift in how state governments can foster sustainable, localized economic development. By adapting the proprietary efficiency of corporate closed-loop systems—the highly coveted "Starbucks Model"—into a heavily regulated, state-run public utility, California can effectively neutralize the extractive friction imposed by the global open-loop credit oligopoly.

Through the rigorous application of Capacity-Based Monetary Theory, the state fundamentally redefines the nature of digital value. It transitions the circulating consumer float from being viewed as a passive, risky liability into a dynamic, sovereign engine for local reinvestment. By executing this economic strategy through the precise legal framework of the Master Agent of the Payee exemption (Financial Code § 2010(l)), and carefully navigating the constitutional Gift of Public Funds doctrine via a firm, legislated commitment to the public purpose, California can build this ecosystem without triggering the regulatory tripwires that have historically suffocated decentralized commercial networks.

Supported by the advanced, high-throughput technical capabilities of PostgreSQL for high-velocity settlement and Fireblocks MPC for secure, DFAL-compliant custody, and intelligently safeguarded by Hamilton Regime-Switching AI, the C3N architecture is both highly scalable and deeply resilient. When structurally integrated with the lending expertise of IBank, the constituent outreach of CalOSBA, and the consumer accessibility of the CalAccount program, the network forms a comprehensive, frictionless public economy.

Ultimately, by framing this highly technical initiative as a populist defense of Main Street against Wall Street hidden fees, California can secure the political mandate necessary to launch the C3N at the ballot box. In doing so, the state will create an unprecedented sovereign wealth engine, funded entirely by capturing the displaced friction of the legacy financial system, thereby securing a prosperous, resilient, and autonomous future for California's independent economy.

-

SME Business Plan

2023 SENATE FINANCE AND TAXATION SB 2217 - North Dakota Legislative Branch, accessed February 19, 2026, https://ndlegis.gov/sites/default/files/resource/68-2023/library/sb2217.pdf

GL Committee Hearing Transcript for 02/21/2013 - C G A, accessed February 19, 2026, https://www.cga.ct.gov/2013/gldata/chr/2013GL-00221-R001300-CHR.htm

California Governor's Office of Business and Economic Development (GO-Biz) - CA.gov, accessed February 19, 2026, https://business.ca.gov/

California Economic Development Leaders Launch New Tool Connecting Business Owners with Trusted Lenders, accessed February 19, 2026, https://www.ibank.ca.gov/california-economic-development-leaders-launch-new-tool-connecting-business-owners-with-trusted-lenders/

About GO-Biz, Leadership Accountability Report, accessed February 19, 2026, https://business.ca.gov/about/about-go-biz/

MUNICIPAL BANK FEASIBLITY TASK FORCE PREP MATERIALS ..., accessed February 19, 2026, https://sftreasurer.org/sites/default/files/2019-08/Mtg.%202_3-20_Municipal%20Bank%20TF%20Prep%20Materials.pdf

Sovereign wealth funds: What they are and why accounting firms should get familiar with them | OnPay, accessed February 19, 2026, https://onpay.com/ledger/sovereign-wealth-funds-swf-summary/

California Small Business Loan Guarantee Program - City of Tracy Economic Development, accessed February 19, 2026, https://thinkinsidethetriangle.com/business-assistance/business-resources/small-business-resources/p/item/18252/california-small-business-loan-guarantee-program

San Francisco Public Bank Coalition Moves Ahead, accessed February 19, 2026, https://publicbankinginstitute.org/san-francisco-public-bank-coalition-moves-ahead/

Gift of Public Funds (Spoiler Alert: It's Illegal), accessed February 19, 2026, https://www.cacities.org/Resources-Documents/Member-Engagement/Professional-Departments/City-Attorneys/Library/2016/Annual-2016/10-2016-Annual_Forbath_Gift-of-Public-Funds_Spoile.aspx

California Code, Financial Code - FIN § 2010 - Codes - FindLaw, accessed February 19, 2026, https://codes.findlaw.com/ca/financial-code/fin-sect-2010/

Political Action - California Business Roundtable, accessed February 19, 2026, https://www.cbrt.org/political-action/

Bill Text: CA AB80 | 2021-2022 | Regular Session | Chaptered - LegiScan, accessed February 19, 2026, https://legiscan.com/CA/text/AB80/id/2386049

California Enacts Sweeping New Law Targeting Money Transmitters | Insights, accessed February 19, 2026, https://www.venable.com/insights/publications/2010/10/california-enacts-sweeping-new-law-targeting-money

2024 California Code Financial Code - FIN DIVISION 1.2 - MONEY TRANSMISSION ACT CHAPTER 2 - Exemptions Section 2010. - Justia, accessed February 19, 2026, https://law.justia.com/codes/california/code-fin/division-1-2/chapter-2/section-2010/

AB 1365 - Assembly Bill Policy Committee Analysis - California, accessed February 19, 2026, https://abnk.assembly.ca.gov/system/files/2025-04/ab-1365-analysis.pdf

Small Business, Innovation & Entrepreneurship, accessed February 19, 2026, https://business.ca.gov/resources/small-business-innovation-and-entrepreneurship/

AB 1365: CalAccount Program. - Digital Democracy, accessed February 19, 2026, https://calmatters.digitaldemocracy.org/bills/ca_202520260ab1365

Public Bank LA: Home, accessed February 19, 2026, https://publicbankla.org/

Agent of Payee Exemption - DFPI - CA.gov, accessed February 19, 2026, https://dfpi.ca.gov/rules-enforcement/laws-and-regulations/opinion-letters-by-law-subject/agent-of-payee-exemption/

Agent of Payee – Payment Processing - DFPI - CA.gov, accessed February 19, 2026, https://dfpi.ca.gov/rules-enforcement/laws-and-regulations/opinion-letters-by-law-subject/agent-of-payee-payment-processing/

Bill Text: CA SB1525 | 2023-2024 | Regular Session | Chaptered - LegiScan, accessed February 19, 2026, https://legiscan.com/CA/text/SB1525/id/3013751

Agent of Payee - DFPI - CA.gov, accessed February 19, 2026, https://dfpi.ca.gov/rules-enforcement/laws-and-regulations/opinion-letters-by-law-subject/agent-of-payee/

Who Is an Agent of a Payee in California? With Rulemaking Pending, Possible Scope Suggested by Opinion Letters - Cooley, accessed February 19, 2026, https://www.cooley.com/news/insight/2021/2021-03-29-who-is-an-agent-of-a-payee-in-california

FIN - Comment Letter on CA Payee Agency - DFPI, accessed February 19, 2026, https://dfpi.ca.gov/wp-content/uploads/sites/337/2019/05/PRO-07-17-Financial-Innovation-Now.pdf

To Gift or Not to Gift: A Primer on Public Funds - FCMAT, accessed February 19, 2026, https://www.fcmat.org/publicationsreports/gift-of-public-funds-acbo-presentation-10-29-24.pdf

7.3 Prohibition of Gift of Public Funds - California Debt Financing Guide, accessed February 19, 2026, https://debtguide-api.treasurer.ca.gov/guide-pages/chapter-7-additional-requirements-imposed-on-issuers-of-municipal-debt/7-3-prohibition-of-gift-of-public-funds

In An Historic Move, California Paves Way For Public Banks - Lozano Smith, accessed February 19, 2026, https://www.lozanosmith.com/news/cnb/CNB862019.pdf

GO-Biz Webinar - Overview of California's Small Business Loan Guarantee Program, accessed February 19, 2026, https://www.youtube.com/watch?v=oJ2dQK4GG5g

Business and Labor | Office of Senate Floor Analyses, accessed February 19, 2026, https://sfa.senate.ca.gov/annualdigests/2011/business-and-labor

county treasurer or the board of supervisors, as the case may be, shall be to safeguard the - SFBOS.org, accessed February 19, 2026, https://sfbos.org/Modules/ShowDocument.aspx?documentid=39680

Public Banking Initiatives March Onward in California | American Postal Workers Union, accessed February 19, 2026, https://apwu.org/news/public-banking-initiatives-march-onward-california/

Lawsuits & Settlements | Page 9 | State of California - Department of Justice - Office of the Attorney General, accessed February 19, 2026, https://oag.ca.gov/new-press-categories/lawsuits-settlements?page=8

The Uncertain Future of the Corporate Contribution Ban - ValpoScholar, accessed February 19, 2026, https://scholar.valpo.edu/cgi/viewcontent.cgi?referer=&httpsredir=1&article=2368&context=vulr

Dark Money: Forcing Public Disclosure - Reclaim the American Dream, accessed February 19, 2026, https://reclaimtheamericandream.org/success-disclose/

RGS Executive Committee Meeting Packet - May 16, 2024 - Regional Government Services Authority, accessed February 19, 2026, https://www.rgsjpa.org/wp-content/uploads/2015/09/2024-05-16-Agenda-Packet-ADA.pdf

See “Ratings” herein - Controller's Office | SF.gov, accessed February 19, 2026, https://sfcontroller.org/ftp/uploadedfiles/mopf/r2c4_OS_SF_General_Hospital.pdf

Innovative IBank Provides California With An Edge - Sunstone Management, accessed February 19, 2026, https://www.sunstoneinvestment.com/innovative-ibank-provides-california-with-an-edge/

CPBA Legislative Briefing 2025 - California Public Banking Alliance, accessed February 19, 2026, https://capublicbanking.com/wp-content/uploads/2025/03/CPBA-Legislative-Briefing-2025-1.pdf

IBank Announces Additional Funding to Support Its Expanding Venture Capital Access Program | California Governor's Office of Business and Economic Development, accessed February 19, 2026, https://business.ca.gov/ibank-announces-additional-funding-to-support-its-expanding-venture-capital-access-program/

AB 258: Economic development: small businesses: Small Business Information Act: internet web portal. | Digital Democracy, accessed February 19, 2026, https://calmatters.digitaldemocracy.org/bills/ca_202320240ab258

Small Business Resources - Advocacy - California Chamber of Commerce, accessed February 19, 2026, https://advocacy.calchamber.com/small-business/small-business-resources/

Technical Assistance for Capital Readiness Program | California Office of the Small Business Advocate (CalOSBA), accessed February 19, 2026, https://calosba.ca.gov/for-calosba-partners/technical-assistance-for-capital-readiness-program/

California SBDC - Business, Better. - Guidance for Small Business Growth, accessed February 19, 2026, https://www.californiasbdc.org/

SSBCI | California Infrastructure and Economic Development Bank (IBank) - CA.gov, accessed February 19, 2026, https://www.ibank.ca.gov/small-business/ssbci/

About CA Loan Match, accessed February 19, 2026, https://www.caloanmatch.org/about-us

In California, a Movement for Locally Controlled Finance Gains Ground | Nonprofit Quarterly, accessed February 19, 2026, https://nonprofitquarterly.org/in-california-a-movement-for-locally-controlled-finance-gains-ground/

PUBLIC BANK LOS ANGELES CAMPAIGN UPDATES, accessed February 19, 2026, https://publicbankla.org/public-bank-los-angeles-campaign-updates/

Eliminating Barriers to Bank Accounts: How CalAccount Can Ensure Financial Inclusion and Serve as a Model for Public Banking - Roosevelt Institute, accessed February 19, 2026, https://rooseveltinstitute.org/publications/eliminating-barriers/

Public Banking | Rise Economy, accessed February 19, 2026, https://rise-economy.org/public-banking/

U.S. Crypto Custody Rules: New Standards & What's Ahead | Fireblocks, accessed February 19, 2026, https://www.fireblocks.com/blog/u-s-crypto-custody-rules-whats-next

Bill Text: CA AB39 | 2023-2024 | Regular Session | Chaptered - LegiScan, accessed February 19, 2026, https://legiscan.com/CA/text/AB39/id/2845913

California Becomes Latest State to Regulate Digital Assets - Morgan Lewis, accessed February 19, 2026, https://www.morganlewis.com/pubs/2023/11/california-becomes-latest-state-to-regulate-digital-assets

California digital assets compliance roadmap: Licensing and annual requirements - BPM, accessed February 19, 2026, https://www.bpm.com/insights/california-digital-assets-compliance/

California Legislature now on the spot in high-stakes poker game - Consumer Watchdog, accessed February 19, 2026, https://consumerwatchdog.org/energy/california-legislature-now-spot-high-stakes-poker-game/

Wall Street vs. The Regulators: Public Attitudes on Banks, Financial Regulation, Consumer Finance, and the Federal Reserve | Cato Institute, accessed February 19, 2026, https://www.cato.org/survey-reports/wall-street-vs-regulators-public-attitudes-banks-financial-regulation-consumer

City Considers a Public Bank - Los Angeles Business Journal, accessed February 19, 2026, https://labusinessjournal.com/featured/city-considers-a-public-bank/

CalBusPAC - Advocacy - California Chamber of Commerce, accessed February 19, 2026, https://advocacy.calchamber.com/elections/calbuspac/

The People V Wall Street: California's Public Banking Shake-Up, accessed February 19, 2026, https://aflep.org/the-people-v-wall-street-californias-public-banking-shake-up/

Ballot Initiatives | State of California - Department of Justice - Office of the Attorney General, accessed February 19, 2026, https://oag.ca.gov/initiatives

An Analysis of the Financial Services Bailout Vote, accessed February 19, 2026, https://ciaotest.cc.columbia.edu/journals/cato/v31i1/f_0021599_17862.pdf

PFMA praises House committee vote to provide businesses and consumers swipe fee relief - Pennsylvania Food Merchants Association, accessed February 19, 2026, https://www.pfma.org/news-blog/pfma-praises-swipe-fee-relief/

Community Banking in the 21st Century, accessed February 19, 2026, https://www.csbs.org/sites/default/files/2024-06/CBRC%20pubs/CBRCReport2013.pdf

SB 478 - Hidden Fees | State of California - Department of Justice - Attorney General, accessed February 19, 2026, https://oag.ca.gov/hiddenfees

California Law Bans Hidden Fees for Goods and Services Starting July 1, 2024 | Insights, accessed February 19, 2026, https://www.hklaw.com/en/insights/publications/2024/06/california-law-bans-hidden-fees-for-goods-and-services-starting-july

California's Ban on Drip Pricing Begins July 1, 2024, accessed February 19, 2026, https://www.pillsburylaw.com/en/news-and-insights/ca-drip-pricing-ban.html

Tom Steyer vows to cut electricity bills by 25%, but experts say the details fall short, accessed February 19, 2026, https://calmatters.org/politics/2026/01/governor-steyer-electricity-rates/

Governor Newsom signs bills curbing billionaire influence on elections and protecting elections from interference, accessed February 19, 2026, https://www.gov.ca.gov/2025/10/02/governor-newsom-signs-bills-curbing-billionaire-influence-on-elections-and-protecting-elections-from-interference/

The Surprising Survival—So Far—of the Corporate Contribution Ban, accessed February 19, 2026, https://businesslawreview.uchicago.edu/print-archive/surprising-survival-so-far-corporate-contribution-ban

Vote Forward, accessed February 19, 2026, https://votefwd.org/

Reform CA Sends 2 Million Texts for Voter ID and to Fight Prop 50, accessed February 19, 2026, https://www.reformcalifornia.org/news/reform-ca-sends-2-million-texts-for-voter-id-and-to-fight-prop-50

Get Out the Vote Phone & Text Banking, accessed February 19, 2026, https://www.nonprofitvote.org/wp-content/uploads/2021/10/Script-GOTV-Phone-and-Text-Banking.pdf

News | Rise Economy, accessed February 19, 2026, https://rise-economy.org/news/

Promote the Vote California, accessed February 19, 2026, https://www.sos.ca.gov/elections/promote-vote-ca

Political Party Statements of Purpose - California Secretary of State, accessed February 19, 2026, https://www.sos.ca.gov/elections/political-parties/party-statements