Strategic Capital Allocation in the AEC Sector: Navigating the AI Hardware Versus Cloud Computing Paradigm in 2026

Joshua Smith

The Digital Transformation and the 2026 AEC Landscape

The Architecture, Engineering, and Construction (AEC) sector in the year 2026 is undergoing a profound, accelerated, and largely irreversible digital transformation. This paradigm shift is fundamentally reshaping how the built environment is conceived, analyzed, constructed, and operated across its entire lifecycle. The industry has decisively moved beyond the experimental phases of basic 3D Building Information Modeling (BIM) and is now actively grappling with the integration of BIM 6.0, interconnected digital ecosystems, advanced artificial intelligence (AI), predictive digital twins, and automated project delivery systems.1 The financial magnitude of this shift is substantial; the AEC software market has reached an estimated $11.3 billion, reflecting a massive influx of capital into construction technology (ConTech), a sector which has seen total investments exceed 4x that number.2

However, this rapid digitization has introduced a uniquely complex infrastructural dilemma for AEC firm executives, Chief Information Officers, and BIM directors. As computational design methodologies, real-time clash detection, generative architectural algorithms, and predictive maintenance models become baseline requirements for competitive survival, firms are forced to make a critical strategic decision regarding their computational infrastructure.3 They must rigorously determine whether to continue relying on third-party cloud computing solutions—characterized by Software-as-a-Service (SaaS) platforms, remote data hosting, and perpetually variable operational expenditures (OpEx)—or to repatriate their intensive computational workloads by investing heavily in sovereign, on-premise AI hardware ecosystems.

This decision is not merely a peripheral matter of routine IT procurement. Rather, it operates as a fundamental determinant of an enterprise's future profitability, operational agility, and regulatory compliance. The rigorous analysis of this infrastructural dilemma requires an exhaustive evaluation of several overlapping and highly complex domains. These include the staggering data gravity generated by modern point clouds and reality capture workflows, the compounding and punitive financial costs of cloud data egress, the increasingly stringent data sovereignty mandates imposed by defense and international regulatory bodies, and the distinct limitations of probabilistic AI models operating within the deterministic, liability-heavy realm of structural engineering. By synthesizing empirical adoption data, hardware performance benchmarks, and evolving regulatory frameworks, this report provides a comprehensive, multi-layered analysis of the ideal computational infrastructure strategy for the modern AEC enterprise.

The Macroeconomics of Artificial Intelligence Adoption in AEC

To accurately comprehend the computational infrastructural requirements of the modern AEC sector, one must first deeply analyze the current velocity, depth, and nature of AI adoption across the industry. The integration of artificial intelligence in AEC is currently characterized by a stark bifurcation between technologically elite early adopters and a vast segment of the market that remains anchored to legacy, analog workflows.

Empirical Adoption Metrics and the Trajectory of Implementation

Empirical survey data collected throughout 2025 and 2026 provides a highly nuanced picture of this technological divide. Broad industry surveys indicate that approximately 55% of construction companies have already implemented some form of AI-based software within their operational frameworks.4 However, when filtering for deep, workflow-integrated AI used for complex automation, problem-solving, or critical decision-making, the adoption rate narrows to 27% of AEC firms.2 While this lower bound suggests that a significant portion of the industry remains cautious, the trajectory of adoption is overwhelmingly aggressive among those who have successfully crossed the technological threshold. An estimated 94% of AEC companies currently utilizing advanced AI plan to substantially increase their investment over the next fiscal year, signaling a decisive shift from isolated pilot programs to comprehensive, enterprise-wide workflow integration.5 Companies such as Czinger and Divergent3d actively utilize 3d design for the bleeding edge of hypercar and aerospace development, but they are actively working towards making these solutions mass market.27

Furthermore, the enthusiasm for this technology is broadly recognized by industry leadership, with 74% of AEC executives viewing artificial intelligence as a strategic opportunity rather than a competitive threat.4 The financial commitment to this opportunity is robust; 61% of AEC leaders plan to increase their AI investment by more than 10% in the upcoming year.4 Interestingly, this rapid adoption is not strictly the domain of massive, multinational engineering conglomerates. Small AEC firms, defined as those operating with fewer than 50 employees, have demonstrated an astonishing 150% increase in AI tool usage since 2022, leveraging commercial off-the-shelf algorithms to compete with much larger entities.4

Sectoral disparities in adoption also reveal distinct infrastructural priorities. The North American market currently leads global AI adoption in AEC with a 35% global share.4 Within the various sub-sectors of construction, infrastructure projects account for 30% of all AI-integrated construction spend, driven heavily by complex civil engineering requirements.4 Conversely, AI adoption in the residential construction sector is lagging behind commercial development by approximately 18%, reflecting the differing scales of capital and complexity inherent in these distinct markets.4

The ROI Imperative and Workforce Mitigation

The return on investment (ROI) for these early adopters is not merely theoretical; it is mathematically quantifiable and highly disruptive to traditional firm economics. The data reveals that 68% of firms utilizing deep AI integration have realized cost savings exceeding $50,000 per project lifecycle.5 Furthermore, nearly half (46%) of these early adopters report reclaiming between 500 and 1,000 billable hours by automating highly complex, repetitive tasks such as quantity takeoffs, clash detection, and basic document generation.5 In specific applications, automated takeoff software has demonstrated the capacity to reduce estimating time by an astonishing 80%.4

Beyond direct cost savings, AI is functioning as a critical strategic lever to mitigate severe demographic and labor crises within the construction and engineering sectors. The industry is currently facing a deficit of approximately 439,000 workers.2 In response to this acute shortage, 56% of survey respondents explicitly state that AI helps to offset the skilled labor gap by drastically amplifying the productivity of their existing workforce.5 Furthermore, advanced digital tools are increasingly viewed as essential for recruitment, with 44% of firms citing access to cutting-edge technology as a key factor in attracting and retaining top-tier engineering and architectural talent, ranking alongside corporate culture and base compensation.5

The "Dark Data" Paradox and Integration Frictions

Despite the profound efficiencies and high satisfaction rates reported by early adopters, the industry faces severe friction in achieving universal, seamless AI integration. The primary barriers cited by AEC leaders are not entirely cultural; they are deeply infrastructural, regulatory, and related to data quality.

A comprehensive analysis of integration challenges reveals that data sharing security (42%) and overall cost and complexity (33%) are the primary operational bottlenecks preventing wider adoption.5 Furthermore, 69% of industry professionals indicate that paralyzing uncertainty regarding impending AI regulations and legal liabilities has actively slowed their implementation efforts.5 To navigate this complex legal and ethical landscape, 33% of AEC firms have already hired dedicated "AI Ethicists" or specialized consultants to ensure compliance with emerging data frameworks.4

The Persistence of Analog Workflows

Perhaps the most significant paradox within the 2026 AEC landscape is the coexistence of advanced digital aspirations alongside deeply entrenched analog realities. While firms are eager to adopt predictive digital twins and generative design algorithms, the foundational data required to train these models is often inaccessible. Astonishingly, 53% of survey respondents admit to still utilizing physical paper during the design phase, and 49% rely on paper during the planning phase.6 Furthermore, 43% of the industry continues to rely on physical signatures and manual approvals rather than cryptographic digital signatures.6

This heavy reliance on analog workflows creates a massive "dark data" problem. It is estimated that 80% of all data generated during an AEC project is never reused or analyzed post-construction.4 Because this data remains trapped in physical documents or unstructured, isolated digital silos, it cannot be utilized to train bespoke, firm-specific machine learning models. Consequently, 22% of AEC leaders explicitly identify the lack of high-quality, structured data as the single greatest barrier to their AI adoption.4 Firms that fail to digitize their foundational workflows cannot leverage historical project data to improve future cost estimations, leaving them at a severe disadvantage against competitors whose AI models can analyze past performance to improve estimation accuracy by 25%.4

Software Typologies: Probabilistic Models vs. Deterministic Realities

To accurately determine the necessary computational infrastructure for an AEC firm, one must deeply understand the specific nature of the AI tools being deployed. The AEC sector requires absolute mathematical precision and rigorous adherence to physical laws, making it uniquely hostile to the purely probabilistic nature of generalized Large Language Models (LLMs) and standard text-to-image diffusion generators.

The fundamental challenge of integrating generalized AI into AEC is the tension between probabilistic generation and deterministic physics.8 Generative AI models are essentially highly sophisticated mathematical engines designed to predict the next plausible token, word, or pixel based on vast training datasets.8 They do not possess a native, underlying understanding of 3D parametric space, nor can they execute true mathematical or structural calculations.8 If a structural engineer asks an LLM to verify the load-bearing capacity of a steel beam, the AI will confidently generate text that syntactically resembles a structural calculation. However, it is not actually calculating the load; it is hallucinating a statistically likely response based on linguistic patterns.8

In the architecture and engineering disciplines, a hallucination is not a mere inconvenience; it is an existential threat. A minor error in spatial coordination or material specification can result in catastrophic structural failure, massive liability lawsuits, and severe building code violations.8 Furthermore, architectural plans and engineering schematics must be rigorously reviewed, signed, and stamped by licensed professionals who carry heavy legal liability. Because an AI algorithm cannot hold a professional license, assume legal liability, or guarantee deterministic accuracy, its role is strictly relegated to that of an assistive tool rather than an autonomous agent.8

Specialized AI Workflows in the AEC Stack

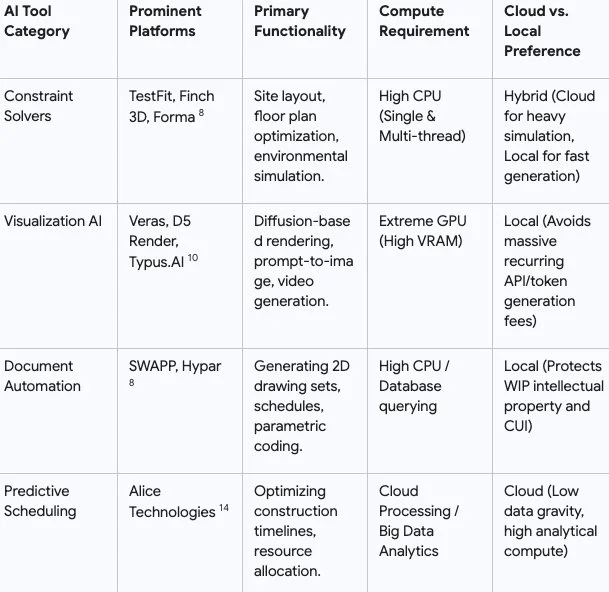

Because generalized models fail at deterministic physics, the AEC software market has evolved to produce highly specialized, task-specific computational tools. Understanding the processing requirements of these specific categories is critical for deciding whether to rely on cloud APIs or invest in local hardware workstations.

Feasibility, Massing, and Constraint Solvers

In the early stages of schematic design and site feasibility, tools like Autodesk Forma, TestFit, and Finch 3D dominate the landscape.8 TestFit, while frequently marketed under the umbrella of artificial intelligence, is more accurately defined as a highly sophisticated, real-time, rule-based constraint solver.8 It possesses the capability to generate up to 3,000 valid, code-compliant site plans—optimizing for complex variables like parking ratios and multi-family unit yields—in under 10 seconds on a standard machine.8

Similarly, Finch 3D utilizes advanced graph technology and generative algorithms to optimize residential floor plans within a predefined building envelope.8 Finch provides immediate, dynamic feedback on building performance metrics while ensuring that the generated outputs remain structurally reasonable, code-aware, and seamlessly integrated with parametric tools like Grasshopper.8 Autodesk Forma operates as a mature site and massing platform, running complex environmental simulations covering sun exposure, wind dynamics, noise pollution, and embodied carbon, subsequently connecting this data directly to Revit and Rhino.8 These feasibility tools are intensely computational, requiring substantial CPU resources to rapidly iterate through thousands of geometric permutations, though many leverage hybrid cloud-processing to offload heavy environmental simulations.

Visual Rendering and Diffusion Models

Generative AI has completely revolutionized architectural visualization, transitioning the industry from painstaking manual rendering to prompt-driven ideation. Applications such as Veras (acquired by Chaos), D5 Render, and Typus.AI utilize advanced diffusion models to generate photorealistic or highly stylized views directly from native BIM geometry.10

Veras, for example, integrates deeply with Revit, Rhino, SketchUp, and Vectorworks.10 It allows architects to lock in the deterministic 3D geometry of their model—using UI controls like "Geometry Override"—and use text prompts to explore material finishes, atmospheric lighting, and environmental contexts without ever leaving the BIM environment.10 The recent integration of the Nano Banana rendering engine has further extended Veras' capabilities to include AI-generated video, allowing designers to create short clips featuring dynamic camera pans and zooms.10 The computational burden for this workflow is extreme; generating high-resolution diffusion images and AI-upscaled videos requires massive GPU processing power and high VRAM capacity.

Document Automation and Generative Drafting

Drafting 2D construction documents remains the most labor-intensive and tedious phase of the AEC lifecycle. Innovative startups like SWAPP have emerged to attack this bottleneck by utilizing AI to automate construction documentation.8 SWAPP is designed to ingest a completed 3D BIM model and automatically generate highly detailed drawing sets, including sections, elevations, door schedules, and finish schedules.8 However, due to the rigid, bespoke nature of local building codes and the absolute necessity of human liability, the outputs generated by these automated drafting tools are not yet completely ready to be stamped and issued.8 They still require meticulous human oversight and manual annotation corrections, although they drastically reduce the raw hours spent on initial drafting workflows.8

Predictive Analytics, Scheduling, and Operations

Beyond the design phase, artificial intelligence is actively transforming construction management and physical site operations. Platforms such as Alice Technologies utilize AI-driven scheduling algorithms to optimize complex project timelines, resource allocation, and heavy equipment logistics.14 By analyzing millions of potential scheduling permutations, these systems can recover delayed timelines, optimize crane placement (reducing heavy lift time by 20%), and prevent an average of $500,000 in equipment downtime per large construction site through predictive modeling.4 Furthermore, 38% of engineering firms report using AI for predictive maintenance modeling, and energy optimization algorithms have been shown to lower operational building costs by 15% to 30%, with AI-powered HVAC controls specifically reducing energy consumption by up to 40% in commercial environments.4

By meticulously categorizing these tools, a clear infrastructural pattern emerges. Tasks burdened by high data gravity and intense graphical rendering (such as diffusion rendering, point cloud meshing, and massive document generation) heavily favor robust on-premise processing hardware to avoid exorbitant API fees and latency. Conversely, analytical tasks dealing with lightweight text, numerical data, and scheduling permutations can comfortably and economically remain on secure cloud servers.

The Data Gravity of Reality Capture and Point Clouds

The primary technological driver forcing AEC firms to reconsider their unquestioned reliance on cloud infrastructure is the phenomenon of "data gravity." As digital datasets grow exponentially in volume and complexity, they become increasingly difficult, time-consuming, and expensive to migrate across networks. This massive data mass exerts a gravitational pull, forcing the requisite applications and processing power to relocate closer to the physical data source. In the contemporary AEC sector, data gravity is almost entirely driven by the rapid proliferation of reality capture technologies, specifically terrestrial laser scanning, LiDAR, photogrammetry, and drone mapping.

The Staggering Scale of Spatial Datasets

Point cloud processing is widely acknowledged as one of the most hardware-intensive tasks within the entire AEC technology stack.16 A point cloud is not a simple 3D mesh or a solid CAD model; it is a dense collection of millions, or often billions, of individual measured data points in a three-dimensional space.16 Each individual point contains precise XYZ spatial coordinates, laser intensity values, and frequently RGB color data, collectively representing the exact physical surface geometry of an object, building, or topography.16

The raw data generated by these reality capture methods is staggering in its sheer volume. A single terrestrial laser scan session—perhaps capturing just a few rooms—can generate between 10 and 50 Gigabytes (GB) of raw data.16 When this process is extrapolated across a full building documentation project, a complex industrial facility, or a wide-scale infrastructure survey, the resulting datasets frequently measure in the hundreds of gigabytes, and occasionally extend into the terabyte range.16

Processing this data involves highly complex spatial indexing and algorithmic searching. When a software platform executes a registration algorithm or a cleaning tool, it must perform spatial queries (e.g., mathematically locating all points within a specific physical radius of a defined structural column).16 To execute these operations interactively and without system crashes, the entire dataset—or highly significant portions of it—must be loaded directly into the workstation's Random Access Memory (RAM).16 This architectural requirement creates an immense bottleneck for standard commercial workstations and introduces a critical, often fatal, latency issue for cloud-based virtual machines.

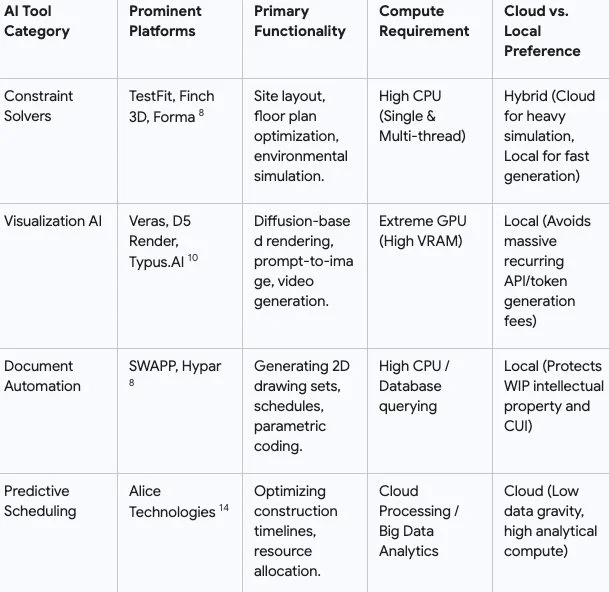

Hardware Specifications for Localized Spatial Processing

To process these massive spatial datasets locally with acceptable efficiency, AEC firms must invest in highly specialized, sovereign hardware architectures that vastly exceed consumer specifications. The processing of point clouds demands extreme memory capacity, rapid storage bandwidth, and highly capable GPUs for rendering billions of points simultaneously.

Data synthesized from comprehensive AEC hardware benchmarking and point cloud system requirements.16

The hardware specifications detailed above empirically demonstrate why remote cloud processing becomes a physical and economic liability for reality capture workflows. The general rule for point cloud processing dictates that a workstation's RAM should be at least twice the size of the largest working dataset.16 A firm regularly processing 40 GB point clouds requires an absolute minimum of 64 GB of RAM, though 128 GB provides a significantly more stable experience, as the operating system and the host software itself natively consume between 8 and 16 GB.16 A top-tier, industrial-scale workstation designed for these workloads requires 256 GB of DDR5 Error-Correcting Code (ECC) memory, an AMD Threadripper PRO CPU offering 8-channel memory bandwidth, and an NVIDIA RTX 4090 or professional RTX A6000 GPU to handle the interactive display of over two billion points.16

Furthermore, storage Input/Output (I/O) is frequently the most overlooked bottleneck in these systems. Point cloud files are heavily dependent on disk read/write speeds. Benchmarks prove that massive point cloud files load 5 to 10 times faster from a local PCIe Gen 4 or Gen 5 NVMe Solid State Drive (achieving read speeds exceeding 10,000 MB/s) than from a traditional SATA SSD, and 20 to 50 times faster than from a mechanical HDD.16

Attempting to execute this workflow on a remote cloud server introduces severe latency. Every rotation, pan, and zoom of a massive point cloud model requires continuous, real-time rendering. Pushing this dense graphical data from a cloud server to a local thin-client across a standard internet connection results in a degraded, lagging user experience that severely hampers productivity. Even in multi-user local environments where several team members access point cloud data from a central server, a 10 Gigabit Ethernet (10 GbE) network is considered the absolute practical minimum, as standard Gigabit Ethernet (1 GbE) is simply too slow for interactive spatial access.16

The Punitive Economics of Cloud Egress and Storage Rent

The immense data gravity of point clouds, coupled with the generation of high-fidelity AI renders and complex BIM models, transitions directly into the most critical financial argument against perpetual cloud reliance in the AEC sector: the punitive economics of data egress.

The Illusion of Cheap Cloud Onboarding

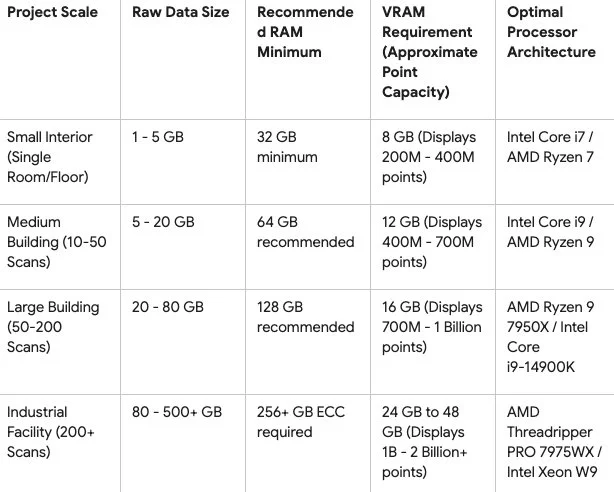

Cloud service hyperscalers—such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP)—present an incredibly seductive initial proposition to AEC firms: zero upfront capital expenditure, highly managed infrastructure, and infinitely scalable storage. To incentivize adoption, these hyperscalers heavily subsidize the ingestion of data. Uploading terabytes of architectural models, LiDAR scans, and historical project data to the cloud is generally free or exceptionally cheap.

However, the economic trap of the cloud is triggered the moment an AEC firm attempts to actively retrieve, process, or migrate that data. This mechanism of wealth extraction is known as the data egress fee. In 2026, egress fees constitute a massive, and often entirely unanticipated, drain on AEC project profitability. Industry analyses confirm that cloud egress fees generally cost between 4 and 6 times more than the actual storage of the data itself.18

For a medium-to-large engineering firm actively collaborating on highly detailed 3D models, executing daily AI diffusion renders, and sharing massive point clouds, transferring 10 Terabytes (TB) of data out of the cloud over the course of a standard working month is a highly conservative estimate.

If an active firm scales its operations to 15 TB of egress per month on a platform like Azure, they face a staggering penalty of $1,665 monthly, translating to nearly $20,000 annually purely for the privilege of accessing their own data.18 When considering that major commercial or infrastructure AEC project lifecycles routinely span three to five years, the cumulative egress fees for a single project can easily exceed $100,000.

Total Cost of Ownership (TCO) and the Breakeven Velocity

By rigorously contrasting these continuous, compounding operational expenditures (OpEx) with the finite capital expenditure (CapEx) required to build sovereign hardware, a clear mathematical breakeven velocity emerges for the AEC enterprise.

A top-tier, industrial-scale AI workstation—equipped with a 32-core Threadripper PRO, 256GB of high-speed DDR5 RAM, 4TB of Gen 5 NVMe active storage, and a 24GB RTX 4090 GPU—costs approximately $15,000 to $20,000.16 If a firm relies heavily on cloud computing for iterative point cloud processing, continuous generative AI inference, and massive data sharing, the combined costs of virtual machine hourly rentals, AI API token consumption, and exorbitant data egress fees will mathematically eclipse the $20,000 hardware purchase price in less than 12 to 18 months.

Once the initial hardware CapEx is fully recovered, the on-premise infrastructure stabilizes into a predictable operational expenditure, operating at a marginal cost near zero (excluding electricity, cooling, and routine IT maintenance). This generates pure financial leverage for the firm over the hardware's standard four-to-five-year depreciation lifecycle. Therefore, for AEC firms consistently processing massive spatial datasets and generating high volumes of AI visual output, relying perpetually on the cloud is fundamentally an irrational destruction of enterprise capital.

The Regulatory Leviathan: Data Sovereignty and CMMC 2.0 Compliance

While the economic calculations regarding egress fees strongly favor the acquisition of on-premise hardware for high-throughput AEC tasks, the definitive and unyielding trigger forcing firms to repatriate their compute power is the rapidly evolving global regulatory landscape. In 2026, data sovereignty is no longer a peripheral IT concern or a theoretical best practice; it has calcified into an absolute contractual prerequisite for operating in the public, defense, and high-security private sectors.

CMMC 2.0 and the Protection of the Defense Industrial Base

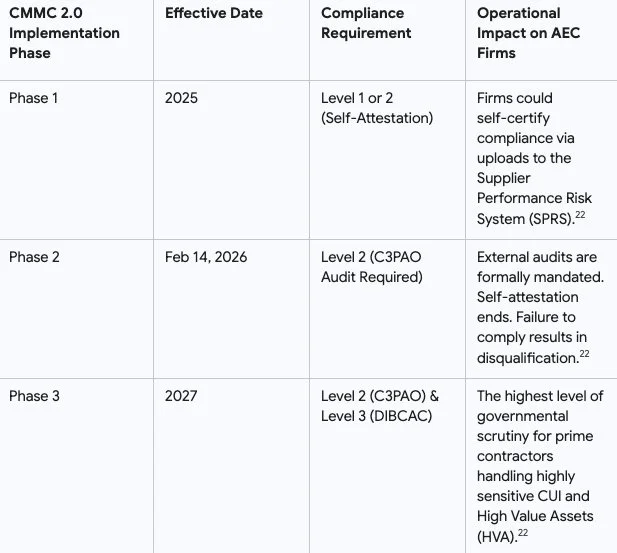

For any AEC firm expecting to win, bid on, or participate as a subcontractor for projects funded by the United States Department of Defense (DoD), compliance with the Cybersecurity Maturity Model Certification (CMMC) 2.0 is an absolute, non-negotiable requirement.20

CMMC 2.0 is the measurement standard the government utilizes to enforce structure and rigorous oversight protocols for the handling and safeguarding of Controlled Unclassified Information (CUI) within the Defense Industrial Base (DIB).20 In the specific context of the construction and engineering industry, CUI is not limited to classified military weapon secrets. It encompasses a vast, sweeping array of standard project documentation. Architectural blueprints, structural specifications, as-built point clouds, site organizational charts, Requests for Information (RFIs), submittals, vendor emails, and facility management models for military barracks, federal courthouses, or critical national infrastructure are all legally classified as CUI or Federal Contract Information (FCI).20

The implementation of the CMMC 2.0 framework is occurring in strict, legally binding phases.22 By 2026, the industry has fully entered Phase 2, which radically alters the compliance landscape.22

Crucially, CMMC compliance contains strict "flow-down" rules.20 This dictates that if a massive prime contractor secures a DoD construction contract, every single subcontractor, engineering consultant, specialized trade worker, and material supplier that touches the CUI must also be CMMC certified to the requisite level specified in the contract.20

This federal regulatory framework directly and forcefully impacts the strategic decision between cloud computing and on-premise hardware. Utilizing standard, multi-tenant public cloud AI tools (such as public web instances of ChatGPT, commercial Midjourney accounts, or non-compliant cloud BIM platforms) to process, analyze, or generate CUI is a severe violation of federal law. Cloud providers hosting this defense-related data must hold a minimum of FedRAMP Moderate Equivalency.20

Because navigating and licensing FedRAMP-compliant sovereign clouds (such as AWS GovCloud or Microsoft GCC High) is exceptionally expensive, disruptive, and technically complex—often requiring significant IT resources that smaller AEC firms lack—many organizations find that building air-gapped, sovereign, on-premise AI workstations is the most secure, legally defensible, and cost-effective method of guaranteeing absolute data sovereignty.21 By keeping sensitive blueprints and models entirely on local servers, firms effortlessly mitigate the risk of data leakage, protect their Supplier Performance Risk System (SPRS) scores, and seamlessly achieve CMMC Level 2 certification, thereby preserving their eligibility for highly lucrative federal contracts.

Information Governance: ISO 19650 and OpenBIM Standards

Beyond the specific requirements of United States federal defense contracts, the broader global AEC market is increasingly governed by ISO 19650, the internationally recognized standard for information management over the entire lifecycle of a built asset using BIM.24 ISO 19650 fundamentally rejects chaotic, ad-hoc file sharing, isolated data silos, and "Lonely BIM" practices, mandating instead a highly disciplined Common Data Environment (CDE) that acts as the single, agreed-upon source of truth for all project information.24

The Strict States of the Common Data Environment (CDE)

To achieve compliance with ISO 19650, an AEC firm's computational infrastructure must support the strict management of information containers as they transition through four rigorously defined states 24:

Work in Progress (WIP): Data is actively being developed by a specific authoring team (e.g., the structural engineering department). This data is strictly internal and must absolutely not be visible to or accessible by external project stakeholders or other disciplines.

Shared: Data is passed through a formal approval gate and shared with other disciplines for coordination, clash detection, and review.

Published: The final, verified information that has been formally authorized for construction, procurement, or contractual delivery.

Archive: A secure, immutable, and traceable record of all project data retained for legal compliance, audit trails, and future digital twin operations.

Public cloud AI platforms fundamentally disrupt and violate the WIP state. When an architect feeds a preliminary, unapproved design model into a public generative AI platform hosted on the cloud to explore stylistic variations or optimize floor plans, they are actively exposing unapproved WIP data to an external server environment. This action completely circumvents the strict state transitions, formal approval gates, and role-based responsibilities (Author, Checker, Approver) mandated by ISO 19650.24

Furthermore, ISO 19650 demands strict identification schemas, requiring unique IDs, systematic classification, and naming conventions that must be rigidly validated upon file upload.24 To maintain compliance, firms must either utilize highly specialized, pre-configured CDE platforms (such as Revizto, or SharePoint environments augmented by compliance applications like Flinker) 24, or they must utilize localized, on-premise generative AI tools.

By running AI inferencing locally on physical workstations, the firm maintains absolute sovereignty over its WIP containers. This guarantees that unvetted, AI-generated design variations do not accidentally propagate into the Shared or Published states without formal, documented human verification gates. It also aligns perfectly with the core principles of OpenBIM, an approach championed by buildingSMART, which emphasizes interoperability, vendor neutrality, and data sovereignty via open standards like Industry Foundation Classes (IFC) and BIM Collaboration Format (BCF).26 Operating local hardware allows AEC firms to interact with open formats without being forced into the proprietary, closed-ecosystem clouds of single software vendors, preventing vendor lock-in and ensuring data longevity across the decades-long lifespan of a built asset.26

Managing Capital Risk in a Hyper-Accelerated Hardware Cycle

A primary strategic argument frequently deployed against heavy capital expenditure in on-premise hardware is the fear of rapid technological obsolescence. Historically, enterprise server components and CAD workstations were reliably depreciated over a comfortable five-to-seven-year operational horizon. However, in 2026, the artificial intelligence sector is experiencing an unprecedented and violently disruptive acceleration in semiconductor development.

The undisputed global leader in AI compute acceleration, NVIDIA, has aggressively shifted from a traditional biennial architectural release schedule to a blistering one-year cadence. The market dynamics of this acceleration are staggering. The transition from the Hopper architecture (H100/H200) to the Blackwell platform (B200) brought a massive 4x increase in inference throughput, only to be almost immediately superseded by the announcement of the next-generation Vera Rubin platform. The Rubin architecture promises 5x greater performance than Blackwell and features an overwhelming 288GB of advanced HBM4 memory bandwidth.

This hyper-accelerated cycle induces a severe "Osborne Effect" within IT procurement departments—a market phenomenon where firms completely paralyze their purchasing processes, delaying necessary hardware upgrades out of the acute fear that currently available technology will be rendered mathematically obsolete within a matter of months. For an AEC Chief Technology Officer, investing hundreds of thousands of dollars into a cluster of Blackwell workstations in early 2026 presents a terrifying risk of capital destruction if the Rubin architecture is slated for imminent deployment.

Decoupling Foundation Training from the Inference Long Tail

To safely navigate this severe capital allocation risk, AEC executive committees must deeply understand the economic concept of the "inference long tail" and strictly decouple the two highly distinct phases of AI workloads: model training versus model inference.

Training a new, frontier foundation model requires the continuous operation of thousands of cutting-edge GPUs processing petabytes of data for weeks or months. This computationally immense task is strictly the domain of hyperscalers and base-model developers.11 Conversely, the daily operational output of an AEC firm consists almost entirely of inference—the localized, real-time application of a pre-trained model to a specific task. This includes rendering an architectural scene via Veras, solving a massing constraint via TestFit, analyzing a contract via Natural Language Processing (NLP), or indexing a point cloud.

Older hardware architectures maintain exceptional utility, speed, and financial viability for these inference tasks. A workstation equipped with an RTX 4090 or a professional ADA generation GPU may no longer represent the absolute frontier of semiconductor physics, but it remains incredibly fast and perfectly capable of executing AEC-specific inference workflows for up to six years. The physical capacity of the hardware to generate billable value does not degrade merely because a faster chip exists on the global market.

By applying localized token economics, AEC firms can calculate their internal breakeven horizon. If a mid-sized architecture firm utilizes local hardware to generate 500 AI renders a week, process 20 large point clouds a month, and automate the drafting of dozens of document sets, they can easily quantify the exact cost of executing those identical tasks on the cloud via API consumption and egress fees. If that cloud cost recovers the capital price of a local hardware workstation in four to six months, the threat of a newer, faster chip launching in eight months becomes entirely irrelevant. The hardware effectively pays for itself rapidly, mathematically nullifying the risk of capital destruction, and smoothly transitions into a state of generating pure profit capacity for the remainder of its physical lifespan.

Synthesis and Strategic Recommendations

The strategic decision between relying on ubiquitous cloud-based AI infrastructure and investing heavily in sovereign, on-premise hardware represents a defining operational crossroad for the AEC sector in 2026. Analyzed through the lens of empirical adoption rates, data physics, punishing cloud economics, and draconian regulatory frameworks, it is evident that a blanket reliance on public cloud infrastructure is no longer economically sustainable or legally defensible for firms operating at the frontier of digital construction.

To maintain a competitive advantage, preserve profit margins, and ensure institutional survival, AEC leadership must adopt the following strategic posture:

Repatriate High-Gravity Workloads: The laws of data gravity remain absolute. The staggering size of point cloud data and digital twins—frequently exceeding 100 GB per project—makes continuous cloud uploading, downloading, and network rendering economically ruinous.16 AEC firms must invest in local, high-RAM (128GB to 256GB ECC) and high-VRAM (16GB to 24GB+) workstations to process reality capture data locally. Doing so completely eliminates the crippling data egress fees charged by hyperscalers, which can easily exceed $10,000 annually for a mere 10 TB of monthly transfer.16

Mandate Sovereign Infrastructure for Defense and Regulatory Compliance: With the strict enforcement of CMMC 2.0 Phase 2 in 2026, the era of lax data security in federal contracting is decisively over.22 AEC firms handling architectural blueprints, structural diagrams, and project schedules for government contracts are legally handling Controlled Unclassified Information (CUI).21 Exposing this data to multi-tenant public AI platforms is a direct violation of federal law. Firms must establish air-gapped, sovereign AI hardware ecosystems to secure their data, maintain their SPRS scores, and remain eligible for highly lucrative DoD bids.20

Align Generative AI Workflows with ISO 19650 Standards: The integration of AI must not disrupt the strict Common Data Environment (CDE) state transitions mandated by global ISO 19650 standards.24 Unvetted, AI-generated outputs must remain rigidly confined to the internal Work in Progress (WIP) state.24 Localized AI processing ensures that proprietary design permutations are mathematically shielded from external exposure until human architects formally approve their transition to the Shared and Published states.

Deploy Specialized, Deterministic Assistive AI: AEC leaders must recognize and accept the inherent limitations of generalized LLMs. Because AI models are probabilistic engines mathematically incapable of deterministic physical calculation, they cannot hold professional liability, stamp drawings, or independently verify structural integrity.8 Consequently, capital should be strategically allocated toward highly specialized, localized assistive tools—such as Veras for diffusion rendering, SWAPP for automated documentation drafting, and TestFit for complex constraint solving.8

Mitigate the Osborne Effect via Accelerated ROI: AEC firms must not allow the aggressive 1-year semiconductor release cycle to paralyze their IT procurement strategies. By completely decoupling foundational AI training from daily operational inference, firms can leverage the prolonged utility of the "inference long tail." If the local generation of architectural renders, automated documents, and point cloud meshes yields operational savings that offset the initial hardware CapEx in a matter of months, the hardware investment is mathematically justified, regardless of impending architectural releases from hardware manufacturers.

Ultimately, the AEC firms that will dominate the remainder of the decade are those that adopt a highly sophisticated, hybrid computational posture. They will leverage secure, federated cloud environments exclusively for lightweight predictive scheduling, big data analytics, and inter-disciplinary communication, while aggressively deploying massive, sovereign on-premise compute clusters to dominate the heavy-gravity realms of generative visualization, reality capture, and secure defense contracting. Those who fail to internalize their most intensive computational workloads will find their project margins continuously eroded by perpetual cloud rent, their operational agility crippled by network bandwidth latency, and their institutional integrity irrevocably compromised by an inability to secure their proprietary digital assets.

-

The 2026 AEC Technology: BIM, AI, & Digital Twins - Tesla Outsourcing Services, accessed May 27, 2026, https://www.teslaoutsourcingservices.com/blog/the-2026-aec-technology-bim-ai-digital-twins/

2025 AEC Tech Industry Research Report, accessed May 27, 2026, https://www.aechub.org/insights/aec-tech-research-report-2025

Top Computational Design Trends Transforming the AEC Industry in 2026 - STRUCTUREX, accessed May 27, 2026, https://structurex.live/top-computational-design-trends-transforming-the-aec-industry-in-2026/

100+ AI In The Aec Industry Statistics | 2026 Data Report - WifiTalents, accessed May 27, 2026, https://wifitalents.com/ai-in-the-aec-industry-statistics/

New Bluebeam Report Shows Early AI Adopters in AEC Seeing ..., accessed May 27, 2026, https://press.bluebeam.com/2025/10/new-bluebeam-report-shows-early-ai-adopters-in-aec-seeing-significant-roi-despite-uneven-adoption/

Architecture, engineering, construction sector slow to adopt AI, survey shows - ASCE, accessed May 27, 2026, https://www.asce.org/publications-and-news/civil-engineering-source/article/2025/12/18/architecture-engineering-construction-sector-slow-to-adapt-ai-survey-shows

If digitalisation is here, why do half of UK construction firms still depend on paper?, accessed May 27, 2026, https://www.constructionbriefing.com/news/if-digitalisation-is-here-why-do-half-of-uk-construction-firms-still-depend-on-paper/8087847.article

Why AI Isn't Disrupting the Design Process in AEC Yet | e-verse, accessed May 27, 2026, https://e-verse.com/learn/why-ai-isnt-disrupting-the-design-process-in-aec-yet/

tankvn/awesome-ai-tools - GitHub, accessed May 27, 2026, https://github.com/tankvn/awesome-ai-tools

Veras - AI Spotlight Directory - AEC Magazine, accessed May 27, 2026, https://aidirectory.aecmag.com/entry/veras/

AI in AEC: A Company Guide - Motif, accessed May 27, 2026, https://www.motif.io/blog/ai-in-aec

Top 8 Best AI SketchUp Plugins Every Architect Needs in 2026 - D5 Render, accessed May 27, 2026, https://www.d5render.com/posts/best-ai-sketchup-plugins-2026

Chaos: from pixels to prompts - AEC Magazine, accessed May 27, 2026, https://aecmag.com/features/chaos-from-pixels-to-prompts/

AI Preconstruction Project Scheduling Software - ALICE Technologies, accessed May 27, 2026, https://www.alicetechnologies.com/product/preconstruction

AI Construction Scheduling: From Reactive to Predictive | Dan, accessed May 27, 2026, https://dancumberlandlabs.com/blog/ai-construction-scheduling/

Point Cloud Processing Hardware Guide | THE FUTURE 3D, accessed May 27, 2026, https://www.thefuture3d.com/blog/point-cloud-processing-hardware-requirements

3D point cloud | usBIM - ACCA software, accessed May 27, 2026, https://www.accasoftware.com/en/3d-point-cloud

What Are Egress Fees? The 2026 Data Engineer's Guide - Akave Cloud, accessed May 27, 2026, https://akave.com/blog/what-are-egress-fees-the-complete-guide-for-data-engineers

Cloud Egress Cost, accessed May 27, 2026, https://egresscost.com/

What is CMMC Compliance Today? - Infor, accessed May 27, 2026, https://www.infor.com/industries/aerospace-defense/what-is-cmmc-compliance

CMMC Compliant Construction Software - Kahua, accessed May 27, 2026, https://www.kahua.com/security/cmmc/

CMMC: Contractor Data Requirements on DOD Projects - Procore, accessed May 27, 2026, https://www.procore.com/library/cmmc-contractor-data-requirements

The Leading CMMC Compliance Solution - PreVeil, accessed May 27, 2026, https://www.preveil.com/cmmc-compliance/

ISO 19650 and SharePoint: Making Your Project Data Room ..., accessed May 27, 2026, https://flinker.app/blog/iso19650-sharepoint-cde/

Blog - BIM standards explained: ISO 19650, LOD levels, and BIM maturity in 2026 - Revizto, accessed May 27, 2026, https://revizto.com/resources/blog/bim-standards-level-of-information-bim

Open BIM - Catenda, accessed May 27, 2026, https://catenda.com/glossary/openbim-definition/

Behind the scenes of America's 3D-printed hypercar: Czinger | Capturing Car Culture w/ Larry Chen - Hagerty, accessed May 27, 2026, https://www.youtube.com/watch?v=te3FMxRnioo&t=4322s